Sometimes, good old focus can be a competitive advantage.

We constantly read about companies that have created barriers to entry – through technology, intellectual property, large-scale manufacturing, or sometimes even by throwing a ton of money at a problem. For startups, this barrier to entry is a constant refrain, especially in conversations with potential investors – “What’s your barrier to entry? What asset are you building that’s hard to replicate?”. And this is a hard question with no easy answers, especially for a young company that’s not building a high-tech, proprietary product – a bigger competitor with deeper pockets could appear at the ramparts anytime, and replicate exactly what you’re doing.

But what if just focus on a particular user segment could help you develop a competitive advantage? What if expending all efforts to serve a particular market niche or user segment could help you unearth a resilient barrier to entry?

I read a book called ‘Good Strategy Bad Strategy’ last year and was struck by how insightful it was. I’ve revisited my notes from the book at least twice now, each time capturing a new nuance. It’s a must read for students of strategy, advisors on strategy, and practitioners. Having been all three (in that order, oddly enough), this is right up my alley.

The book had many great ideas on sources of power for companies – what gives a company lasting supremacy in its market. One idea that stayed with me was of single-minded focus – how focus on a particular type of user can be a sustainable source of power or competitive advantage. How would this work? Let’s dig in – this feels like another 1800 word post.

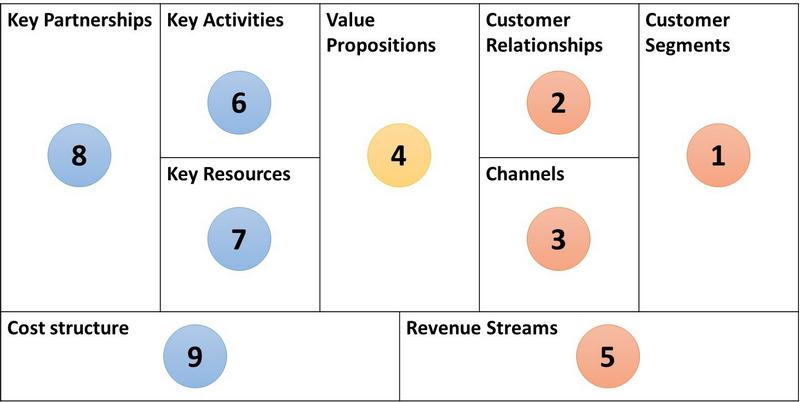

Any company’s business model has 9 different parts, as below:

Source: Strategyzer.com

The author, Richard Rumelt, points out that to focus on a specific user segment, you need to make coordinated changes across multiple or all parts of your business model. Thus, your final offering to the customer is a sum of many moving parts that have all been finely configured – a sum that, as the cliché goes, is more than its parts. Applying such focus takes incredible coordination of policies, which, along with their interlocking and overlapping effects, can then confer unassailable advantages and make you a hard act to follow.

I know this seems very philosophical (a little like bad strategic advice!), so let’s look at a few examples to illustrate this better:

1. IKEA

Rumelt uses the example of IKEA to illustrate this concept. IKEA is a furniture retailer that sells ready-to-assemble furniture. It targets do-it-yourself or DIY users, who love the feeling of putting something together. It has been hugely successful across multiple countries, but 70 years since its founding, no credible competitor has appeared or lasted. That’s sustainable competitive advantage!

IKEA has no secret sauce in terms of patented technologies for furniture, greater marketing strength, etc. The source of IKEA’s lasting advantage is, instead, the coordination between the different elements of its business model to serve its target segment. For a competitor to challenge IKEA, they don’t just have to sell ready-to-assemble furniture – they’ll have to change their whole business model.

- They’ll have to design new types of furniture;

- They’ll have to start carrying larger inventory;

- They’ll have to create their own, branded stores; and

- They’ll have to change their selling models.

Thus, copying IKEA is not a simple matter. IKEA’s policies are so different from the norm in the furniture industry that any competitor would have to replicate ALL of them to meaningfully compete for the same user segment. Adopting one or two of these policies and implementing them, even perfectly, would be useless – it would add huge expenses without providing any real competition.

2. Apple

Apple is another example. Over the years, Apple has targeted its products at premium customers who want a superior experience – well-designed products that just work. They’re not interested in the most technologically advanced products with the most bells and whistles – they want products that do their job simply and well. Oh, and there’s snob value too.

Apple has made several interdependent decisions to target this group:

- Complete ownership of the product: Take the iPhone. Unlike its closest competitor, Android, Apple controls the entire product – the OS, the hardware, user interface, etc. This allows it to deliver a very coordinated and quality user experience.

- Complete ownership of computer ecosystem: Moreover, Apple coordinates the experience across all its products. The Apple ecosystem can satisfy all your computing needs – desktop, laptop, tablet, phone and music player. All of these products follow the same design language, and work together seamlessly – they sync with each other very easily, without any need to fiddle with system settings.

- Branded retail stores with a luxury experience

- Marketing mainly to premium customers who don’t mind spending more – this not only raises product revenue, but also increases the long tail of revenue from app store downloads, music downloads via iTunes, etc.

The reason Apple’s position in the market is unassailable is that a competitor can’t just copy one or two things to start selling to the same group of customers. The competitor would have to copy everything, a formidable task even for very nimble companies. And copying sequentially won’t work – you can’t begin to deliver the Apple or IKEA value proposition without copying everything from the outset, in a coordinated manner. Which is why, even though Android and its partner OEMs have copied a lot of product design elements from Apple (in fact, the first Samsung Galaxy S was an iPhone in all but name), they haven’t been able to displace Apple from its position as the proprietor of all things cool.

Thus, the business models of IKEA and Apple are like a chain – multiple independent elements interlock to engineer a truly durable value proposition. As for a competitor, the flipside of a chain-linked model applies – your proposition is only as strong as your weakest link. Focusing on strengthening just one or two aspects of your model won’t increase your ability to compete even one bit – you need to strengthen everything, all at once.

Let’s try and apply this mental model of a chain to a few other sectors. Are there other companies as well, which have used focused, chain-linked business models to derive competitive advantage?

3. Wal-mart: In the 60s and 70s, Sears and Kmart dominated retail. But they mainly served large towns or cities that could ‘support’ a large retailer. Wal-mart changed the game by creating large-format stores away from cities, allowing enormous spaces at lower costs. It positioned itself as a ‘discounter’, something other players avoided like the plague. And it was able to make money while offering deep discounts, through several interlocking innovations:

- Extremely wide product portfolio with deep discounts on some products, cross-subsidized by other high-margin products

- Cutting-edge technology to track customer purchase behavior, and tailor portfolio accordingly

- Agile supply chain, keeping its stores well-stocked with the right products very efficiently

Thus, several innovations, all focused on offering products at the lowest prices, gave Wal-mart lasting competitive advantage. By 2002, Wal-mart was the largest retailer in the world, and Kmart was bankrupt.

4. Dell: If you wanted to buy a desktop in the US in the 80s or 90s, your only options were to either buy a standard configuration through a retailer, or buy individual PC components to customize the machine yourself. Unless you built the PC yourself, you did not get much choice in the product or configuration you wanted. Dell saw an opportunity to change this by offering customized configurations, and thereby targeting the more technologically adept consumer.

Dell took a number of hard decisions to make this happen. It created an easy to use online / phone interface for users to configure computers of their choice. It delivered this promise through a mass customizing production process, and built a direct-to-customer distribution channel. None of these decisions were easy to replicate even singly, much less in lockstep. The result – a lucrative business model that stood unchallenged during the PC boom of the 90s.

OK, these are standard business school case studies. Let’s look at a few newer companies.

5. Innocent: The British healthy drinks / smoothies player has built a strong position in its home market. Innocent offers health-oriented users very fresh fruit-based drinks – their promise is, zero preservatives, only natural fruit. Offering this focused proposition means a number of business model decisions – sourcing the best fruits only, producing for short shelf life, faster cold chain logistics to get the product to retailer shelves very quickly, and so on. All separate decisions, coordinated to deliver user value. Competitors have found it very hard to replicate this – Pepsico, after years of trying to compete in this market, finally bought a smaller competitor to gain a toehold.

6. Zara: Zara has carved itself a preeminent position in the ‘fresh fashion’ space. Zara’s stores are always stocked with the latest trends – Zara gets clothes from design to outlets in 10-15 days flat. And it has done this by tailoring multiple parts of its operating model to accentuate this speed:

- Much larger design team than other apparel brands – its 200 designers ensure a steady flow of new designs, taking advantage of the latest trends and feedback from customers.

- While most apparel brands manufacture in China, Zara manufactures in Europe close to its main markets – this gives it a head-start of at least 1.5-2 months.

- Short production runs, with limited quantities – Zara doesn’t run more than one production cycle for most of its products. If a particularly striking outfit runs out at its stores, that’s it. You won’t see it again. From a user’s point of view, this drives a purchase decision faster. If you plan to come back tomorrow to buy a dress, it may not be there.

Putting these aspects together, other brands find it very difficult to catch up with Zara – all of these are major business model revamps that are difficult to pull off, whether alone or in coordination with each other.

These and several other successful companies show that focus and coordination can create a massive barrier to entry and lasting competitive advantage, keeping challengers at bay for years to come. It’s a telling reminder to businesses – you don’t need cutting-edge technology or a massive fund-raise, just good old-fashioned customer service will do!

What do you think? Are there any other consequences – positive or negative – of focusing your business model on a specific user segment? Would love to hear from you – mail me at [email protected], tweet at @jithamithra, or comment here on this blog. And do subscribe here – I post roughly once a week, on startups, business models, consumer behavior, etc.

PS. I’ve just started a newsletter called The Startup Weekly with Abhishek Agarwal, a close friend, curating the most interesting articles, case studies, etc. for startups that we come across every week. Would be a good addition to your inbox (so much for conquering it). Sign up here – first issue goes out this Saturday!

2 Responses

Comments are closed.