Zero to One is a powerful book, that changed how I thought about entrepreneurship. I’ve written about the importance of the Power Law before, and what it means for what you choose to do.

(Check out the book on Amazon here.)

To get more such book summaries every week, along with other great reads on startups, business, and tech, don’t forget to sign up below.

What do you know that others don’t?

- What valuable company is no one building?

- Creating value is not hard; capturing enough of that value is harder

- In 2012, when the average airfare each way was $178, the airlines made only 37 cents per passenger trip. Compare them to Google, which creates less value but captures far more. Google brought in $50 billion in 2012 (versus $160 billion for the airlines), but it kept 21% of those revenues as profits—more than 100 times the airline industry’s profit margin that year.

- Progress can take one of two forms

- Horizontal or extensive progress means copying things that work—going from 1 to n. Horizontal progress is easy to imagine because we already know what it looks like

- Vertical or intensive progress means doing new things—going from 0 to 1. Vertical progress is harder to imagine because it requires doing something nobody else has ever done. If you take one typewriter and build 100, you have made horizontal progress. If you have a typewriter and build a word processor, you have made vertical progress.

- If you focus on near-term growth above all else, you miss the most important question you should be asking: will this business still be around a decade from now?

- In March 2001, PayPal had yet to make a profit but our revenues were growing 100% year-over-year. When I projected our future cash flows, I found that 75% of the company’s present value would come from profits generated in 2011 and beyond—hard to believe for a company that had been in business for only 27 months. But even that turned out to be an underestimation. Today, PayPal continues to grow at about 15% annually, and the discount rate is lower than a decade ago. It now appears that most of the company’s value will come from 2020 and beyond.

- LinkedIn is another good example of a company whose value exists in the far future. As of early 2014, its market capitalization was $24.5 billion—very high for a company with less than $1 billion in revenue and only $21.6 million in net income for 2012. You might look at these numbers and conclude that investors have gone insane. But this valuation makes sense when you consider LinkedIn’s projected future cash flows.

- The overwhelming importance of future profits is counterintuitive even in Silicon Valley. For a company to be valuable it must grow and endure, but many entrepreneurs focus only on short-term growth.

Thoughts on Monopolies

Monopolies vs. Perfect Competition

- Monopoly is the condition of every successful business

- Under perfect competition, in the long run no company makes an economic profit. Capitalism and competition are opposites. Capitalism is premised on the accumulation of capital, but under perfect competition all profits get competed away.

- If you want to capture value, don’t build an undifferentiated commodity business.

- Non-monopolists exaggerate their distinction by defining their market as the intersection of various smaller markets; monopolists, by contrast, disguise their monopoly by framing their market as the union of several large markets

- In business, money is either an important thing or it is everything. Monopolists can afford to think about things other than making money; non-monopolists can’t.

- If the tendency of monopoly businesses were to hold back progress, they would be dangerous and we’d be right to oppose them. But the history of progress is a history of better monopoly businesses replacing incumbents.

- A monopoly like Google is different. Since it doesn’t have to worry about competing with anyone, it has wider latitude to care about its workers, its products, and its impact on the wider world. Google’s motto—“Don’t be evil”—is in part a branding ploy, but it’s also characteristic of a kind of business that’s successful enough to take ethics seriously without jeopardizing its own existence.

- Winning is better than losing, but everybody loses when the war isn’t one worth fighting.

- Just as war cost the Montagues and Capulets their children, it cost Microsoft and Google their dominance: Apple came along and overtook them all. In January 2013, Apple’s market capitalization was $500 billion, while Google and Microsoft combined were worth $467 billion. Just three years before, Microsoft and Google were each more valuable than Apple. War is costly business

- When Pets.com folded after the dot-com crash, $300 million of investment capital disappeared with it.

- Sometimes you do have to fight. Where that’s true, you should fight and win. There is no middle ground: either don’t throw any punches, or strike hard and end it quickly.

Monopolies and Moats

- Every Monopoly is unique, but they usually share some combination of the following characteristics: proprietary technology, network effects, economies of scale, and branding.

- Proprietary Tech – As a good rule of thumb, proprietary technology must be at least 10 times better than its closest substitute in some important dimension to lead to a real monopolistic advantage. The clearest way to make a 10x improvement is to invent something completely new.

- Network effects: Network effects can be powerful, but you’ll never reap them unless your product is valuable to its very first users when the network is necessarily small.

- Network effects businesses must start with especially small markets. Facebook started with just Harvard students — Mark Zuckerberg’s first product was designed to get all his classmates signed up, not to attract all people of Earth.

- This is why successful network businesses rarely get started by MBA types: the initial markets are so small that they often don’t even appear to be business opportunities at all.

- Economies of scale: A good startup should have the potential for great scale built into its first design.

- Strong brand: other monopolistic advantages are less obvious than Apple’s sparkling brand, but they are the fundamentals that let the branding effectively reinforce Apple’s monopoly.

- Beginning with brand rather than substance is dangerous.

Building a Monopoly as a Startup

- Every startup is small at the start. Every Monopoly dominates a large share of its market. Therefore, every startup should start with a very small market. Always err on the side of starting too small. The reason is simple: it’s easier to dominate a small market than a large one.

- The perfect target market for a startup is a small group of particular people concentrated together and served by few or no competitors. Any big market is a bad choice, and a big market already served by competing companies is even worse.

- It’s always a red flag when entrepreneurs talk about getting 1% of a $100 billion market. In practice, a large market will either lack a good starting point or it will be open to competition, so it’s hard to ever reach that 1%. And even if you do succeed in gaining a small foothold, you’ll have to be satisfied with keeping the lights on: cutthroat competition means your profits will be zero.

- Sequencing markets correctly is underrated, and it takes discipline to expand gradually.

- The most successful companies make the core progression—to first dominate a specific niche and then scale to adjacent markets—a part of their founding narrative (related to Crossing the Chasm – I’ll add book notes soon)

- As you craft a plan to expand to adjacent markets, don’t disrupt: avoid competition as much as possible.

Control over distribution

- Superior sales and distribution by itself can create a Monopoly, even with no product differentiation. The converse is not true. No matter how strong your product—even if it easily fits into already established habits and anybody who tries it likes it immediately—you must still support it with a strong distribution plan.

- In between personal sales (salespeople obviously required) and traditional advertising (no salespeople required) there is a dead zone – the distribution doldrums.

- Suppose you create a software service that helps convenience store owners track their inventory and manage ordering. For a product priced around $1,000, there might be no good distribution channel to reach the small businesses that might buy it.

- Even if you have a clear value proposition, how do you get people to hear it? Advertising would either be too broad (there’s no TV channel that only convenience store owners watch) or too inefficient (on its own, an ad in Convenience Store News probably won’t convince any owner to part with $1,000 a year).

- The product needs a personal sales effort, but at that price point, you simply don’t have the resources to send an actual person to talk to every prospective customer.

- This is why so many small and medium-sized businesses don’t use tools that bigger firms take for granted. It’s not that small business proprietors are unusually backward or that good tools don’t exist: distribution is the hidden bottleneck.

- Suppose you create a software service that helps convenience store owners track their inventory and manage ordering. For a product priced around $1,000, there might be no good distribution channel to reach the small businesses that might buy it.

- Advertising can work for startups, too, but only when your customer acquisition costs and customer lifetime value make every other distribution channel uneconomical.

- Whoever is first to dominate the most important segment of a market with viral potential will be the last mover in the whole market.

- If you can get just one distribution channel to work, you have a great business. If you try for several but don’t nail one, you’re finished.

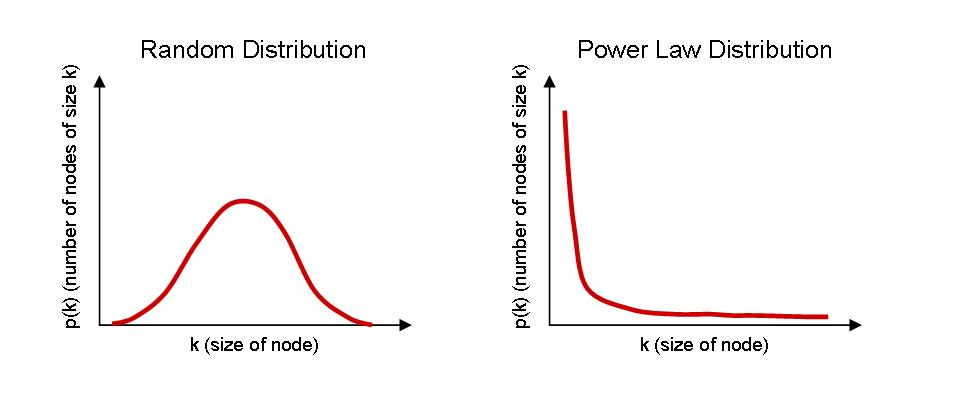

Power Laws (the most interesting part of the book)

Never underestimate Exponential Growth, Compounding, and the Power Law distribution. The Power Law distribution—so named because exponential equations describe severely unequal distributions—is the law of the universe. It defines our surroundings so completely that we usually don’t even see it.

Venture Investing returns are Power Law distributions

- The error lies in expecting that venture returns will be normally distributed: that is, bad companies will fail, mediocre ones will stay flat, and good ones will return 2x or even 4x. Assuming this bland pattern, investors assemble a diversified portfolio and hope that winners counterbalance losers. But this “spray and pray” approach usually produces an entire portfolio of flops, with no hits at all. This is because venture returns don’t follow a normal distribution overall.

- Our results at Founders Fund illustrate this skewed pattern: Facebook, the best investment in our 2005 fund, returned more than all the others combined.

- Palantir, the second-best investment, is set to return more than the sum of every other investment aside from Facebook.

- This highly uneven pattern is not unusual: we see it in all our other funds as well.

- The biggest secret in venture capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund combined.

- This suggests two very strange rules for VCs

- First, only invest in companies that have the potential to return the value of the entire fund. This is a scary rule, because it eliminates the vast majority of possible investments.

- Second: because rule number one is so restrictive, there can’t be any other rules.

- Consider what happens when you break the first rule. a16z invested $250,000 in Instagram in 2010. When Facebook bought Instagram just two years later for $1 billion, a16z netted $78 million—a 312x return in less than two years. That’s a phenomenal return, befitting the firm’s reputation as one of the Valley’s best. But in a weird way it’s not nearly enough, because it has a $1.5 billion fund: if they only wrote $250,000 checks, they would need to find 19 Instagrams just to break even.

- This is why investors typically put a lot more money into any company worth funding; investors who understand power laws invest in as few companies as possible

- The power law means that differences between companies will dwarf the differences in roles inside companies. You could have 100% of the equity if you fully fund your own venture, but if it fails you’ll have 100% of nothing. Owning just 0.01% of Google, by contrast, is incredibly valuable (more than $35 million as of this writing).

What you work on matters far more than doing it well

- Every university believes in “excellence,” and hundred-page course catalogs arranged alphabetically according to arbitrary departments of knowledge seem designed to reassure you that “it doesn’t matter what you do, as long as you do it well.” That is completely false. It does matter what you do. You should focus relentlessly on something you’re good at doing, but before that you must think hard about whether it will be valuable in the future.

- If you do start your own company, you must remember the power law to operate it well

- The most important things are singular: One market will probably be better than all others

- One distribution strategy usually dominates all others, too

- Time and decision-making themselves follow a power law, and some moments matter far more than others

- in a power law world, you can’t afford not to think hard about where your actions will fall on the curve.

Seven questions every business must answer

- The Engineering Question: Can you create breakthrough technology instead of incremental improvements?

- The Timing Question: Is now the right time to start your particular business?

- The Monopoly Question: Are you starting with a big share of a small market?

- The People Question: Do you have the right team?

- The Distribution Question: Do you have a way to not just create but deliver your product?

- The Durability Question: Will your market position be defensible 10 and 20 years into the future?

- The “secret” Question: Have you identified a unique opportunity that others don’t see?

The book also illustrates how very few cleantech businesses have survived, using these seven questions.

To get more such book summaries every week, along with other great reads on startups, business, and tech, don’t forget to sign up below.

Read Next

Book Reviews

- Book Review: Zero to One, Slate Star Codex

Related Articles / Blog Posts

- The Power Law, or why working hard is not enough

- Winners don’t do things differently. They do different things.

- The rise of the superstars, The Economist

- Power Laws in Venture, Jerry Neumann

- John Seabrook and the Modern Song Machine, Farnam Street

- The scale of tech winners, Benedict Evans