Over the last few years, I’ve been quite interested in the startup investing process.

At the trivial level, understanding the investing process could help struggling entrepreneurs (like me) raise funding faster. And, assuming that this investing philosophy does pick winners, this could also teach us what kinds of businesses tend to make it big. And we could then apply those patterns to our own businesses.

Marc Andreessen wrote a landmark article in 2007, on the only thing that matters. If you haven’t read it, go do so now. I’ll wait.

I re-read this article every few months. One line stood out to me the first time itself (and every time since).

He channels Andy Rachleff (Co-founder of Benchmark Fund, one of the most successful VCs) in his article, saying:

When a great team meets a lousy market, market wins.

When a lousy team meets a great market, market wins.

When a great team meets a great market, something special happens.

Thus, of the three key dimensions of a startup opportunity – market, product and team – market is far and away the most important aspect.

What’s the takeaway for an entrepreneur? Take aim at a humongous market, and put your head down and execute.

But is that true? Is targeting a large market the only important factor? Are the team, technology, etc. not as important?[1]

[fancy_box id=6][content_upgrade id=500]BONUS: Do you want this article as an easy-to-read PDF?[/content_upgrade][/fancy_box]Is large market the most important factor?

It certainly is, according to the conventional wisdom. According to Andy Rachleff, again:

The best investments have high technical risk and low market risk. Market risk causes companies to fail. In other words, you want companies that are highly likely to succeed if they can really deliver what they say they will.

Don’t take market risk – i.e., aim for markets that are already large. Instead, take tech risk – where the product itself is hard to create.

This sounds great, and is a commonly accepted truism. And it also seems to be common sense.

But, again, is it true?

One way to settle this is to look at the performance of venture capital over time. As they say, nothing talks like money. But a quick look at VC returns can be quite sobering.

The Kauffman Foundation reports that VC hasn’t outperformed public markets since the late 1990s. In fact, since 1997, VCs have returned less cash to investors than they invested!

Could it be that this VC approach of taking high tech risk but low market risk isn’t working?

Tech matters (more)

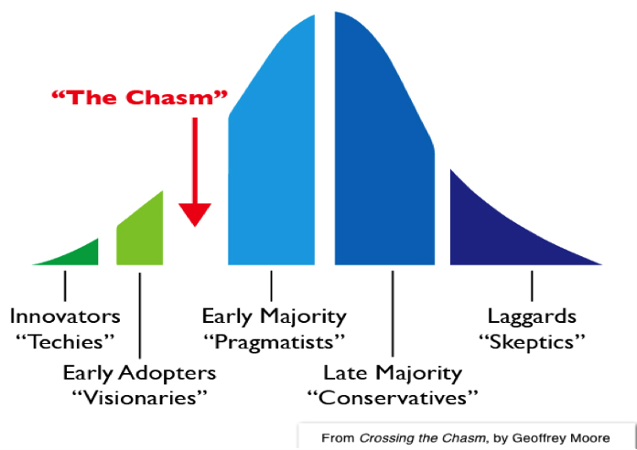

I’ve just finished reading Crossing the Chasm, Geoffrey Moore’s landmark book. He presents technology adoption as a bell curve, with a few “gaps” between segments.

It’s easy to get the innovators and the early adopters. They want to be the first to try new technologies, so they’re primed to be convinced. You start hitting the main market only with the next group, the early majority.

Moore’s key insight is that it’s not natural to move from the innovators and the early adopters to the early majority. That’s why there’s such a huge chasm between these segments in the image above. A graveyard of companies that show great early traction, but suddenly hit a wall and collapse into the chasm.

His model suggests two pointers for technology companies:

- Building a version of the tech, and serving innovators and early adopters, comes first.

- The real challenge is crossing the chasm. You need to find a specific application to solve the early majority’s existing problems. This market isn’t visible or obvious at first – you need to create / discover it.

Thus, tech companies don’t take tech risk. They take market risk. If they find a big market, they succeed big. If they don’t, they fail.

Jerry Neumann has written an excellent history of venture capital in the 80s. He makes a few similar observations (I paraphrase):

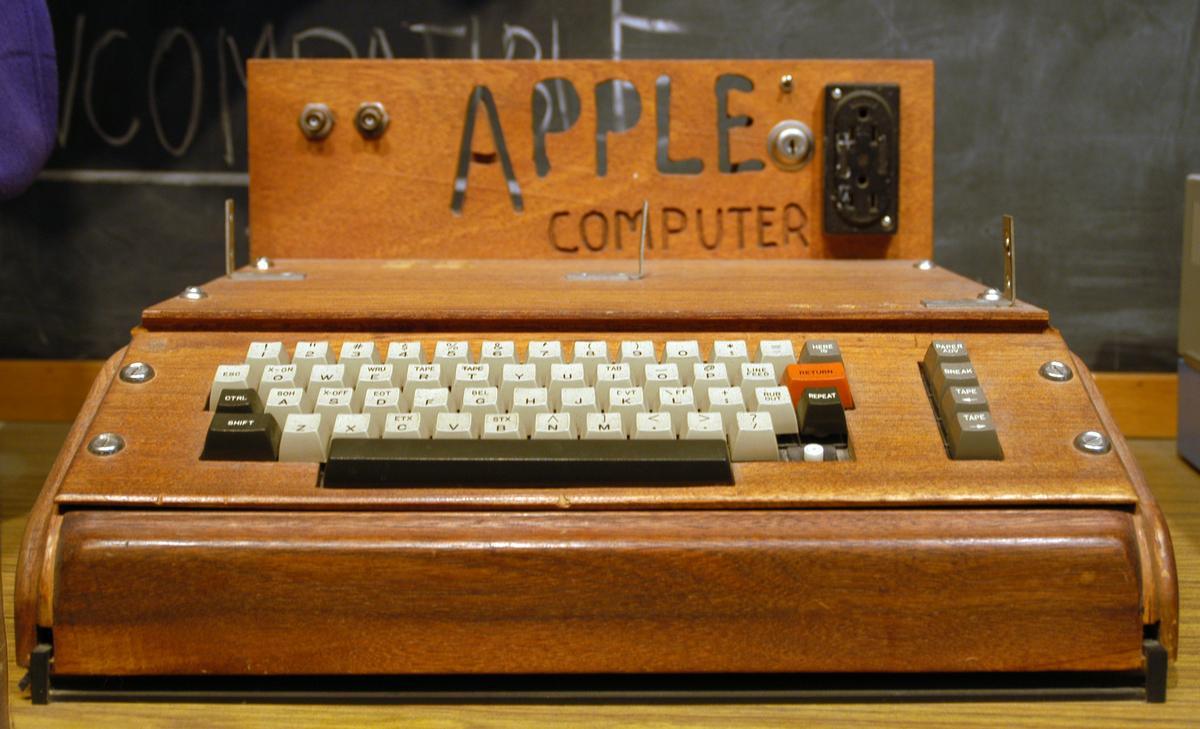

- Whenever VC returns peaked, the driver was high market risk. Would there be a big market for computers (60s, Intel)? Would there be a big market for PCs (70s, Apple, Microsoft)? Would biotech become big (Genentech)? Would the Internet reach the masses, or would it remain a plaything of the elite (90s)?

- These markets may seem inevitable today, but that’s just hindsight bias. Ask Ken Olsen. Or Thomas Watson. Or anyone in this article.

- In most cases, investors didn’t take tech risk. Often, they found already-working products. Apple’s technology was already working when it raised funding.

- Whenever VCs tried to reduce market risk to stabilize returns, they failed. For example, in the 80s, they entered more traditional, massive industries like retail. Result: returns were consistent and stable. But bad.

Thus, VCs didn’t often take tech risk. They preferred technologies that were already proven, and showed promise. And whenever they tried to reduce market risk by entering existing large markets, they failed.

At the end, Jerry summarizes:

The only thing VCs can control that will improve their outcomes is having enough guts to bet on markets that don’t yet exist. Everything else is noise.

Peter Thiel’s Founders Fund adds its own voice to the argument. It highlights how, from the 60s to the 90s, VC was a predictor of the future. Today, though,

VC has ceased to be the funder of the future, and instead has become a funder of features, widgets, irrelevances. In large part, it also ceased making money, as the bottom half of venture produced flat to negative return for the past decade.

When you focus on incremental innovation, for a market that’s here and now, returns fall.

And last, Paul Graham makes a similar point, even more indirectly:

When something is described as a toy, that means it has everything an idea needs except being important. It’s cool; users love it; it just doesn’t matter. But if you’re living in the future and you build something cool that users love, it may matter more than outsiders think. Microcomputers seemed like toys when Apple and Microsoft started working on them… The Facebook was just a way for undergrads to stalk one another.

I alluded to a similar point in a previous article, where I said that you must target a deep need for a narrow population, rather than a shallow need for a broad one.

[fancy_box id=5][content_upgrade id=430]BONUS: Get my checklist to identify bad startup ideas that sound good[/content_upgrade][/fancy_box]What about the team, then?

As a VC friend of mine was quick to remind me when we discussed this, the quality of the team is incredibly important!

But this quality is not theoretical or bookish. It’s not about which Ivy League school you graduated from. Or even whether you have a string of successes under your belt (at least in consumer).

Instead, it’s about three things:

- How driven you are. Will you overturn that 99th stone to find the gold mine? Or will the first 2-3 pivots fatigue you? Your initial ideas for tackling a problem will rarely be right. You’ll need to persist: find a new beachhead, and wade in again.

- Are you willing to learn? Again, you won’t be right the first time. They say industry knowledge is a great unfair advantage. True, but it’s also a double-edged sword.

- Can you execute?

So what’s the conclusion?

Which of these three is the most important?

The ex-consultant in me would answer, “all three”. And he’d throw in an “it depends” for good measure.

But it appears the conventional VC wisdom, of taking tech risk but not market risk, is wrong. As the Founders’ Fund article above says, the current trend of funding incremental innovations and more efficient solutions for existing markets is what has pushed VC returns downwards.

And what does this mean for entrepreneurs? Instead of trying to build something for large markets that VCs seem to be interested in, “swing for the fences”. But not in the conventional sense of aiming for large markets. Instead, try and piggy back on emerging trends that could become waves.

Sure, you’ll probably strike out. But should the market materialize, you will laugh all the way to buying the bank.

I’d love to hear your opinions. If you’re an entrepreneur or startup investor – what’s your stand on market risk vs. tech risk? Do email me at mail@jitha.me, tweet at @jithamithra, or comment here. I’d love to publish a follow-up sharing your opinions.

Thanks to Aditi Gupta and Abhishek Agarwal for commenting on drafts of this post.

[1] This article is about VC backable startup, and not a small business in general. Many great cashflow businesses (e.g., auto dealerships, general manufacturing) are often not high-growth businesses that can return 20x on invested capital, and are therefore not VC backable. See this article for a great description of such businesses.