[A version of this article first appeared in The Quint.]

As a seed-stage investor at OperatorVC, I see at least 50 startups a month that are looking to raise a seed round. Most pitches aren’t perfect. That’s usually OK – a founder’s core competency should be building, not pitching.

But one of the most egregious mistakes is calling yourself the “Uber of X”, or the “Airbnb of Y”.

The moment you say this, the pitch ceases to remain credible.

This is such a common refrain – and such a rookie mistake – that I can’t help but point it out.

Startups ain’t Star Trek, but I feel Picard’s pain.

I think the “X of Y” epidemic started with Y Combinator’s application process. The How to Apply page mentions that YC likes hearing “X of Y”. It helps them place the startup into the pantheon of successful companies they’ve seen.

It makes sense for YC. When they have to scour thousands of startups in a short time to select a few, a metaphor helps. “Hi, I’m the Uber of bicycles.” Enough, let’s move on.

But most fundraising pitches are not YC applications or Demo Days. Yet, Paul Graham’s words are gospel. So everyone and their next-door founder has adopted this with great gusto.

Even in situations where it doesn’t make sense.

And it’s gotten to a point where it’s almost ludicrous! I’ve heard a startup describe itself as “the BikeBob of X”. Have you heard of BikeBob? Neither have I! [Note: I’ve disguised the real name of “BikeBob”, but trust me, you haven’t heard of it.]

Let’s be clear – this is not a “done thing”. It’s not a “best practice”. It’s a mistake, in most pitching situations. Even if it’s Uber you’re comparing yourself to, and not BikeBob or MotorcycleMary.

Before digging into why it’s a mistake, there’s an even more basic question. Why do we do it? Fierce individualists that we are, why do we willingly attach our identities to something else?

Why do we do it?

Three reasons:

Helps explain the product. This is why it’s recommended for YC Demo Day.

Shows a pattern. We all know that VCs are in the pattern recognition business. This just makes it easy for them to realize that you’re the next Uber. They better chase you with their money!

An attractive narrative. Starting up is hard. It’s difficult to justify to your family – and yourself – why you’re abandoning a stable ship. In such a scenario, who wouldn’t like a little ego boost?

Saying you’re Uber of X is awesome. Wouldn’t you love to equate your startup to a unicorn?

But the moment I hear it in a startup pitch, it’s hard not to cringe. Why?

Why is it a mistake?

1. Gives the impression that you’re not solving a real problem.

It sounds like you just read about a successful startup’s business model, and applied it to the first sector you could think of.

“AirBnb for cars: rent other people’s cars when they aren’t using them.”

It’s like you went to the neighborhood workshop and bought yourself a hammer. Now everything looks like a nail!

Unless an idea has formed organically from a real problem, it’s probably a bad startup idea.

[Side note: this is just one characteristic of a startup idea that sounds good, but is probably bad. Click here for a full list of such characteristics.]

“Do you want a bicycle at this very moment?” “Not really, but your speakers look awesome!”

Sometimes, it’s a real problem all right. But the solution doesn’t make sense.

An “Uber of intercity B2B logistics” is OK from a problem perspective. Manufacturing companies do need intercity logistics.

But do they need it on-demand? No! A huge majority of customers transport loads often, on predictable timelines. They’d prefer negotiating longer-term contracts.

I once thought of applying the Airbnb model to books.

Once I finish a book, it’s lying on my bookshelf. Wouldn’t it make sense to lend it out to others who may want to read it?

The problem is real – I need to buy a book to read it. But is this the best solution at scale? No. Not in a world where book prices are falling, e-retailers offer one-day delivery, and you can download a Kindle book in an instant.

Do I know the problem exists? In some cases, yes. In most cases, no. All I know is that the solution has worked. In another, unrelated sector.

2. It can constrain your imagination.

The moment you start calling yourself “Uber of X”, you constrain your thinking. You fool yourself into believing you have a foolproof playbook. When in fact there are important nuances and differences that are critical to consider.

When Taxi for Sure started, one initial focus area was inter-city cabs. Do you think they’d have discovered the lucrative on-demand taxi market if they called themselves the “Redbus of taxis”?

Oyo Rooms, a successful startup in its own right, could have called itself “Airbnb of hotels”. But would that have worked? Would the founder have made the same decisions? It’s possible. But not probable.

3. It’s another stake in the ground you must defend.

VCs are in the business of pattern recognition. They’ve internalized the patterns of successful startups to a level you never will.

They’ll point out nuances of those playbooks that don’t apply in your case.

I once saw a startup that was building the “Oyo of manufacturing”. Just like Oyo helps hotels use their idle capacity, this founder would help manufacturers deploy theirs. Only two tiny chinks in his plan:

Hotels have average capacity utilizations of around 60%. Manufacturers have much higher utilizations. And moreover, they don’t want to be at 100% – flexibility is important. If a plant has 80% utilization, there’s no idle capacity.

Unlike hotels, production is stable. A plant owner doesn’t want one-off users. He’d prefer someone who promises orders for at least 6 months.

Pattern recognition has a flipside too. An average VC sees 500 pitches every year, to select 3-4. So, they’re far more well-versed in the patterns of bad startups than good ones. Be ready for sweeping statements!

VCs are far better at identifying bad startups than good ones.

Fundraising 101. Explain the problem you’re solving. Explain why it’s an important problem to solve. Then show your traction.

Or flip the order, if your traction is more compelling than your problem description.

These are the two most important things, for your investors to make money. They’ll be listening hard.

Not only does this avoid the pitfalls above, it also serves your original reasons better:

1. It’s much easier to explain.

The problem is now self-evident, and there’s a clear line-of-sight from problem to solution.

2. VCs would prefer identifying the patterns themselves.

Let’s say you’re trying to solve a particularly hard logical puzzle. Would you prefer it if your friend told you the answer, or would you rather figure it out yourself?

So it is with investors as well (at least with me). It’s my job to predict the future, and I’ll feel more fulfilled if I detect the pattern myself.

This may not be flamboyant. But it’ll be a better ego boost when a VC tells you that you’re the Uber of X!

TL:DR

Calling your startup “X of Y” while pitching to investors is a mistake.

It sounds like you’re replicating an existing model, rather than making an original attempt to solve a real problem.

It can also constrain your thinking.

Instead, simply state the problem you’re solving and how you’re solving it.

Leave the pattern-recognition to the investors.

PS. A far more insidious version of the “X of Y” template is “X of India”. I’ve written about it in this article.

PPS. I’m calling this “fundraising mistake #7” because (a) there are several other mistakes; and (b) I want to goad myself to put the rest of them down. So watch this space.

Successful entrepreneurs, investors and strategy experts all extol the virtues of focus. I have as well, as a strategy consultant, then a founder, a writer, and now as a seed stage investor at OperatorVC.

“If you focus on a small segment, you can own it, dominate it.”

So the conventional wisdom goes.

But there are times when focus can constrain a startup from achieving its potential. When you become a big fish in a small pond, while there are gloriously large oceans just around the corner.

How do you know which is which? How do you know when to focus, and when to extend?

This came up in a conversation with Ankesh Kothari, a fellow entrepreneur and seed investor. He highlighted how a lot of startups focus too narrowly on a small market, and never expand. And we often see the opposite at OperatorVC. Startups trying to solve problems across a broad swathe of consumers from the outset. “Microsoft Office products that solve everyone’s problems”, as I call them here.

Here’s what’s interesting: neither of these is always the right answer.

Sometimes, you have to focus on a specific consumer segment. Make sure you solve a need deeply. At other times, you need to expand your horizons.

If you focus too acutely, you’ll never become a $100 million company.

This is not intuitive. You can’t be deep in the weeds one moment, and flying at 20,000 feet the next.

Great founders can alternate between these two opposite behaviors well. And legendary founders plan for this in advance.

Before Tesla started, Musk anticipated when he would focus. And when he would extend lower in the price pyramid. And he wrote it all in a badass blog post, for all the world to see.

[Tweet “If you focus too acutely, you’ll never become a $100 million company.”]

So how can you be more like Elon Musk?

At its very basic, it’s three simple steps:

Start with extreme focus. Focus on a narrow segment. Serve that segment’s needs so completely that you build a monopoly in it. Focus on a city, community, or neighborhood, and then OWN it

Then, expand into an adjacent segment

Repeat steps 1 and 2.

Several great startup successes have done exactly this:

Facebook: Started with a student listing, just for Harvard. Once Zuckerberg found product-market fit there, he then expanded to other universities. And then the rest of the world.

Uber: Started as a premium limo service. Only for select customers, only in San Francisco. Today, there’s a good chance you’re reading this sitting in an Uber.

In the 70s, two Harvard geeks built a simple Basic interpreter for the Altair, a decidedly non-popular microcomputer. How would that ever grow big? It did. You might have heard of Microsoft.

Now, I know what you’re saying. Hindsight is 20:20.

Is this just one of those clichés that you retrofit to success stories? Or is there actually a lesson here for people just starting out?

Is it even possible to be more like Elon Musk?

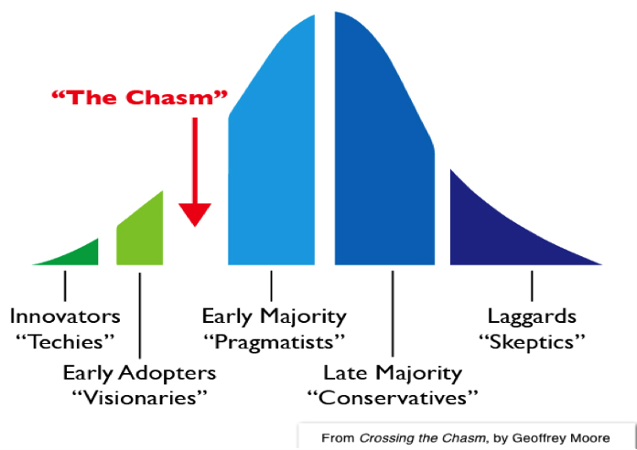

The Chasm model of product adoption is a great framework to know when to focus, and when to extend.

At the trivial level, we all know this. Tech enthusiasts and early adopters will use your product first. The mass market (the Early Majority or “Pragmatists”) will gradually start using it later.

But the Chasm Model offers two new insights:

There’s a “chasm” between the early adopters and the mass market (the early majority). It’s very hard to make that leap, and many startups die trying.

Unlike the early adopters, the early majority aren’t interested in your tech. They are interested in its application to their most important needs.

And therein lies the way.

When to focus

Focus when you’re crossing the chasm.

Focus on a single narrow niche within the mass market. Understand that niche and its most important needs. Create an application of your technology tailored to that segment’s needs. Find product-market fit, and cement your place there. Own that niche.

Let’s take an example we’ve seen at OperatorVC. Say you’re building an AI based system to help people recover from illnesses. Don’t start coding algorithms for all the million diseases that are possible. Don’t even start with the 100 most prevalent diseases. Start with one disease. Just ONE.

When to extend

Extend once you own that first segment.

Select the next niche(s) in the mass market that you want to own. Again, design applications of your technology for those segments.

And REPEAT.

This is exactly what Tesla is doing now, working its way down the price segments.

Once the healthcare bot is perfect for that one disease, it’ll be much easier to expand to the next disease. And the next hundred.

[Tweet “Be like Elon Musk. Focus first. And then extend to own the world.”]

So, when you’re starting off, make sure you focus on a segment you can really own. But also be ready to extend later, so you can own the market.

One year ago, I started the Sunday Reads newsletter. It’s a short email that goes out once every week (on Sunday, obviously), with “the best articles on business, strategy, entrepreneurship, and everything in between.”

Every week, I share the best articles I read that week. Sometimes they’re organized around a theme. Sometimes not. But there they are, without fail, in your inbox every Sunday.

I realized just last week that over the year, I had shared 600+ articles through that weekly email. And often, I read at least ten times as many articles during the week, to choose these best 10-12 articles.

What have I learned from these 6,000+ articles? Have they made me better at what I do?

No trees were harmed in the making of this post

A part of me answers almost immediately – yes, for sure! But how exactly have they helped? Can I tease out the key lessons I’ve learned from the articles? Or is it just a vague sense of achievement and hope – surely I haven’t wasted those hours?

So, over the last 7 days, I went back to those 52 emails. And pulled out the key learnings and principles that I’ve actually tried to use in my life.

Two caveats before we go on:

First, this is a long post. I’ve tried to summarize the key concepts I’ve learned, and it turns out 6,000 articles means a ton of learnings!

Second, I’ve included (several) links for further reading. Every paragraph is a rabbit hole. So, first read through the whole thing without clicking through on any link. Then, come back. Feel free to dive as deep as you want, on the subjects that interest you.

1. Goals don’t work. Use systems instead.

This was not a new lesson for me. But across article after article, book after book, this got reinforced. No matter the field, what seems to work is understanding the basic principles and following them. That’s it.

Success is not about choosing an ambitious goal and stretching to reach it. Whether in running your business or trying to win arguments with your spouse, hard work won’t cut it. Instead, you understand the basics, try a lot of different things, learn what works, and iterate or double down.

If you do it right, then no matter whether you succeed or fail in one specific endeavor, you’ll always come out ahead. You’ll always learn something that’ll be useful next time.

[Tweet “Goals are for losers. Use systems instead.”]

This sounds a little hackneyed at this high level, I know. But as you’ll see, it permeates all the other lessons below.

Further reading:Goals vs. Systems. I’ve read this a few times before, but I was still blown away by the simplicity when I read it just now. If you like this, you’ll love Scott Adams’ book.

2. Growth Mindset vs. Fixed Mindset

There are two types of people – those with a fixed mindset, and those with a growth mindset.

If you have a fixed mindset, you think you are at the peak of your skills. You’re the best artist, manager, husband, wife, etc. you can be.

If, on the other hand, you have a growth mindset, then you strongly believe you can grow and improve at whatever you do. Whether in your personal life (you can always become a better husband. OK, that hit too close to home), or in your professional career. There’s always room for improvement.

Your mindset determines how successful you are to a surprising extent. People with growth mindsets are more willing to try new things, learn new skills, and take risks. And those who take risks, get the rewards. Fortune favors the brave, etc.

Further Reading: You can read Carol Dweck’s book Mindset, which outlines the research on the subject. Or read Maria Popova’s review of the book.

3. Deliberate Practice

Let’s say you have a growth mindset. Is that enough to grow and improve your skills over time?

If the goals vs. systems argument tells us anything, it’s that just believing you can improve at something isn’t enough. So, what’s the system for this?

Practice. Not just doing something for 10,000 hours. Deliberate practice. Working at the edge of your abilities, getting immediate feedback (succeeding / failing), learning, and trying again. That’s what builds skills.

If you want to learn business, start a side-business. At every stage – idea generation, building your first product, selling it to your first customer – you’ll fail the first few times. And you’ll learn immensely.

If you want to improve your writing skills, start a blog. It takes 2 minutes on Medium. Write every day, and ask your friends and colleagues for feedback. Rinse, repeat.

[Tweet “Don’t just practice. Do deliberate practice. That’s how you build skills.”]

Further Reading: Cal Newport’s book on the subject is excellent. This article from his blog is a good summary of the six traits of deliberate practice.

These were the three most important learnings for me from my last year of reading.

Take a systems approach to all your endeavors

There’s always room to become better at what you do

The “system” to become better is deliberate practice

Everything else stems from these key principles. They form the foundation for the rest of the learnings. Get these right, and everything else falls into place. How’s that for a system?

As I continued plowing through the articles, I saw that a lot of them were organized around skills essential to succeed in the workplace today. Communication, structured thinking and problem solving, creativity, and focus (especially focus), to name a few.

How do we build these skills?

4. How to learn anything

Communication, structured thinking, etc. are critical skills. But there’s one skill that’s a precursor to all this – the ability to pick up new skills quickly.

As Scott Adams says in his book, every new skill you learn doubles your chances of success. To take a simple example – an MBA who knows to code is far more valuable than just an MBA. And if this person also understands, say, cinematography, then the unique opportunities available are far more lucrative.

So, you need to continually build new skills throughout your career, to take advantage of new opportunities. And ideally, you’ll build skills that are themselves useful across a diverse set of sectors (system approach again).

[Tweet “Every new skill you learn doubles your chances of success”]

OK, you’re sold. Learning how to learn is key (it’s also the secret moral of Kung Fu Panda, but that’s another story).

But how do you learn? You could join a course at your local university, or hire a teacher online, and do your 10,000 hours.

Or, you could use the Pareto principle to identify the 20% of concepts that have 80% of the importance, and quickly learn and practice those.

Don’t you want to be that guy, who always sees through to the crux of an issue? Who understands the real problem, which no one else can see? Who always sees the way out of an unresolvable predicament?

I certainly want to be that guy.

Turns out, this is a learnable skill.

a. Don’t be stupid

Charlie Munger, Warren Buffett’s partner-in-crime, once said, “The best way to be smart is to not be stupid”.

We are not rational beings, as economists would have us believe. Not by a long shot. As I’ve written before, we’re not only not rational, we’re also irrational in consistent and repeatable ways.

We’re subject to several cognitive biases, which predictably warp our judgement.

Anchoring is one example of a pervasive bias. The first number thrown in a negotiation becomes an unconscious anchor to the rest of the bargaining. That’s why both parties fight to shout out the first bid.

Availability bias is another one. We overestimate the probability of an event if we can remember vivid instances of it. We pay more for earthquake insurance than for calamity insurance (even though the latter includes earthquakes!), we overestimate the possibility of winning the lottery if our neighbor just won it last week, and so on.

How do you avoid these biases? Here’s the thing – you can’t.

Since these operate at a subliminal level, just knowing them won’t prevent them. Next time someone makes the first offer in a negotiation, you’ll predictably bargain around that.

Instead, counteract these in your decision-making by using a two-track thinking process.

First, make a decision rationally (to the best of your abilities)

Then, try and recognize the biases you’re subject to, and adjust accordingly

Do this again and again, and you’ll soon become a natural. At not being stupid.

[Tweet ““The best way to be smart is to not be stupid””]

b. Develop a latticework of mental models

This idea also comes from Charlie Munger.

There are several different frameworks that help us understand the world. Understanding and building a repository of these frameworks in our heads can help us become much faster at comprehending the forces at play around us.

Whenever you read anything interesting or insightful, or see a surprising pattern, put it down in a notebook.

Over time, this will become a repository of the smartest things you’ve read. A surprisingly easy place to go back to whenever you need inspiration, or a way out of a thorny problem.

[Aside: if you want to learn how to have great startup ideas, read this guide. But be warned, you’ll sometimes come up with ideas that seem to have a lot of potential, but are actually bad. Here’s how to recognize bad ideas that look good.]

7. How to communicate better

a. How to write better

Just two rules: (1) Never use passive voice; and (2) Keep it simple. Don’t use two words where one will do. Don’t use a long sentence where two shorter ones will do. That’s it. Nothing more.

(1) First, understand whether your opponent’s opinion is changeable at all. Ask: “What specific data points, if true, would convince you to change your mind?” If nothing will, you might as well not waste your time arguing. [Aside: yes, the similarity to the scientific method is not incidental].

(2) Then, as Daniel Dennett says here, first restate your opponent’s view so clearly and succinctly that they wish they could have put it that way themselves.

(3) Then, call out the specific areas on which you agree with your opponent, and what you’ve learnt from their view.

Then, and only then, should you say even one word of criticism.

And yes, remember Miller’s Law. “To understand what another person is saying, you must assume that it is true and try to imagine what it could be true of.”

Before you say some statement is wrong or silly, first challenge yourself to think of a scenario where that statement actually makes sense. [The same principle applies for criticizing political decisions, competitors’ moves, etc.]

Finally, be happy to be proven wrong, like Darwin. Remember, you only learn when you lose arguments.

[Tweet “Be happy to be proven wrong. You only learn when you lose arguments.”]

c. How to give feedback better

There’s no playbook here.

Actually there is one – sandwich your feedback between two appreciative comments. It’s also known as The Shit Sandwich, and no, it doesn’t work. People see it coming a mile away. You start by saying “Your emails are always so well formatted”, and the opposite person immediately thinks, “God! How have I screwed up now?”

Instead, be authentic.

And come from the right place. Remember, you’re giving feedback so that the person succeeds going forward. And give constructive feedback frequently – don’t wait for review cycles, or the end of the week, etc.

In addition to all these, there’s one more important tenet to interpersonal communication. Always respond positively when someone says something to you. Negative / sarcastic reactions, or even no reaction at all, can be very damaging to relationships, as this article from Farnam Street recounts.

8. How to focus

This is an important one. Between emailing all day, getting pings on Whatsapp, and checking what’s new on Twitter, it’s a wonder we get any work done.

Even as I type this, my hand continually reaches out to check my phone. Maybe there’s a new message since I last checked 2 minutes ago?

As this article from the NYT argues, focus is a critical skill. And it’s incredibly hard in this age of digital distraction. But as Cal Newport shows in his book Deep Work, it can be learned.

How do we learn it? By practicing it:

First, use the Pareto principle. Take your to-do list, and remove the 80% of tasks that are unimportant.

Then, use Parkinson’s Law (“work expands / contracts to fill the time available to it”). Give yourself slightly less time than needed for each of the 20% important tasks. This will force you to focus – if you get distracted, you won’t be able to finish in the given time.

Of course, you’ll have to do the less important tasks at some point. For this, use a shallow work checklist that you tick things off when taking a break from the important tasks.

9. How to become a better manager

Read this FAQ from Henry Ward, CEO of eShares. Enough said.

10. How to get lucky

The last and final lesson I learned, and arguably the most important one. Building all those skills is great – it sets you up for success. But getting all the firewood together in one pile is not enough. Something has to light the fire. And luck is that matchstick.

Analogies apart (you can tell they’re my weak spot), you can acquire all the skills you want and work as hard as you can. But to win really big, you also need Lady Luck to favor you. And luck can be as capricious as they come.

But, like everything else above, you can engineer luck as well. You can expose yourself to positive luck, while limiting the downside from negative luck.

In the words of Nassim Taleb, you can be antifragile.

How do you do that?

a. Employ a barbell strategy – maintain a portfolio of low-risk / low-reward and high-risk / high-reward strategies.

Keep your day job, and try and build a side-business on the weekends. Quit your job only after the startup starts to scale. Even Craigslist was built in Craig’s spare time.

[Extra marks if you build your side business in a Power Law market. In such markets, if you do win, you’ll win huge.]

b. Build a strong network of ‘weak’ links – the best opportunities are at the edges of the status quo in every field. If you know people at the cutting edge in every industry, you’ll be better placed to spot and capitalize on big opportunities. Spend time with A+ people from other industries. [Note: This is also evidently the no. 1 predictor of career success].

c. Develop an “abundance mindset”. Look around and notice things. Be open to serendipity.

Nat Eliason has written a great primer on getting exposure to positive luck. You can also read this excellent book.

That’s it. Those were the lessons I learned from the 6,000+ articles I read in the last 52 weeks.

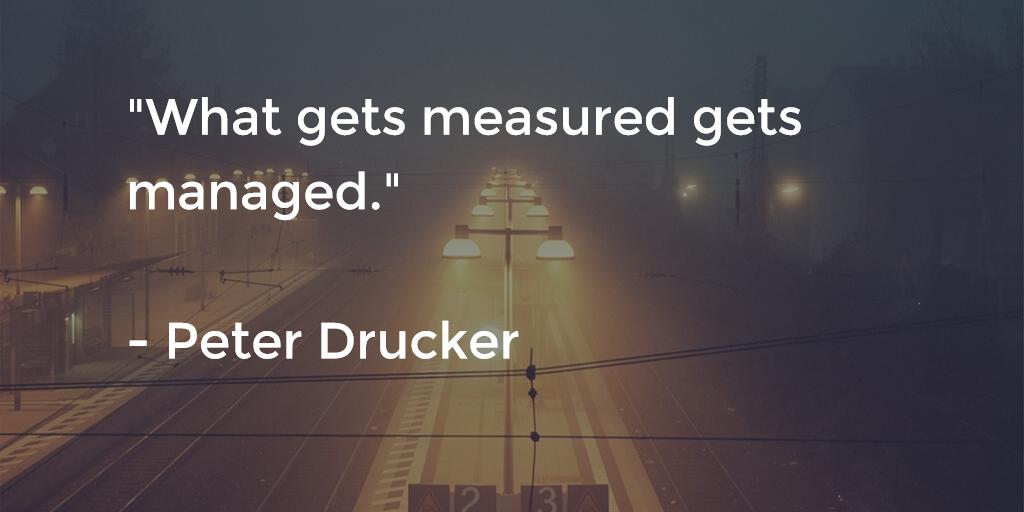

Many of us have heard the saying “What gets measured, gets managed”. A simple, yet powerful thought. With a simple corollary – what doesn’t get measured, doesn’t get managed.

But last week I heard an interesting anecdote that drove home the power of measurement. In reality, the corollary is far more extreme. In the eyes of the person responsible, what doesn’t get measured… doesn’t really exist.

But before we get into that, let’s take a second look at Peter Drucker’s statement.

In just five words, he captures an overwhelming amount of insight. On human behavior, cognitive biases, the power of incentives, and the strength of a goal-driven approach.

If you want something done, measure it. If there’s an objective number representing the outcome of your actions, you (or your team or partner) will automatically work towards improving it. If you’re assessing something subjectively (or not at all), then progress will never happen.

We see scores of examples of this, across our personal and professional lives:

A. Choose an objective metric

If you need to exercise more, then don’t just tell yourself to do that every day. Track your activities. A guy I know walks up and down his office building five times every day, just so he can hit the step goal on his Fitbit.

If you want to increase user engagement on your app, look at your Daily Active Users or Monthly Active Users metrics. Run experiments to increase them. Don’t directly start integrating fun-and-games mechanics without an objective goal.

B. Choose the right metric

If you want to lose weight, don’t just count calories. Instead, count the amount of simple carbs you’re eating. [Aside: this is an excellent layman’s book on the subject].

If you want your salespeople to increase sales, don’t measure the daily hours they clock. Count the amount of sales they make. Else, you’ll have diligent workers… who use Facebook 8 hours a day (9-5, on the clock).

As they say, “track it till you crack it” (it rhymes, so it must be true).

Photo by Russ Hendricks on Flickr (https://bit.ly/32vlBp8)

But I heard a surprising story last week about Indian broadcast media. It underlined the power of the measure, or in business jargon, the Key Performance Indicator (KPI). It showed how, when marketers can’t measure their impact on a market, they all pretend it doesn’t exist. Even though they know full well that the market is substantial.

First, some quick background on the Indian broadcast market.

Traditional audience measurement was flawed

Till recently, TV broadcasters and advertisers in India measured impact of TV programming using an agency called TAM. TAM had special set-top boxes installed in 20K households across India, which tracked data on TV watching habits.

Using this, TAM could tell broadcasters how many people, in which cities, were watching which show. Broadcasters were incentivized to produce content that generated high TAM scores, so they could show this data to advertisers and demand hefty ad rates.

It was a useful KPI, aligning incentives all round. Except for a tiny problem – TAM’s sample was urban-centric. In a market where the rural populace forms a sizeable proportion of TV watchers.

Broadcasters recognized this problem, and fixed it

Since TAM placed disproportionate importance on urban TV viewing, it was clearly unrepresentative. And the powers-that-be knew that. So, in the last two years, the industry created an alternative – the Broadcast Audience Research Council, or BARC.

BARC looks at a much larger sample, including a sizeable rural proportion. The system rolled out just recently, with an objective of giving a clearer picture to broadcasters and advertisers.

Instantly, broadcasters started generating new, “rural-focused”, content

Here’s where it gets interesting.

As BARC launched, more and more shows with supernatural elements started appearing on TV. Even existing shows, whether staid family dramas or comedies, started having occult “tracks”. This is what happened in 2015:

New shows were launched, like Darr Sabko Lagta Hai (“Everyone gets scared”), Naagin (rough translation: “serpent woman”), etc. In fact, Naagin was one of FOUR new shows about serpent-women!

Many ongoing shows started introducing supernatural elements. Not only daily soaps (or saas-bahu shows as we call them in India), but also comedies.

Why did this happen? The reasoning goes – ghosts, serpent-people and others are integral parts of age-old Indian folklore. These beliefs are still a major part of rural lives. Hence we’ve introduced them to create a better connect with the new rural audience.

Disregard the blatant stereotyping for now (we’ll come back to it later). Assuming that this is what the rural audience wants, the logic makes eminent sense.

Why then was television content urban-focused? Why were there no shows targeting the rural populace?

Because rural wasn’t measured.

The only number available was the urban-focused TAM, which was out of step with reality. And producers of TV shows, in full knowledge of this fact, nevertheless used it. There was no other number, so they followed this one. Single-minded and unswerving, like mice following the Pied Piper.

[Tweet “If you can’t measure it, it doesn’t exist.”]

What does this mean for us? We need to be more careful than ever in choosing our KPI – the True North that we set our sails by.

If we don’t choose the right metric (or worse, choose the wrong one), the outcomes will be the antithesis of our objectives. No matter how well-meaning we or our colleagues are.

Coming back to our rural stereotype, we’ll find out how true it is in the coming months. If it isn’t, expect the broadcasters to nimbly eliminate the black magic tracks from their shows. It will be managed adeptly. After all, it’s getting measured now.

Over the last few years, I’ve been quite interested in the startup investing process.

At the trivial level, understanding the investing process could help struggling entrepreneurs (like me) raise funding faster. And, assuming that this investing philosophy does pick winners, this could also teach us what kinds of businesses tend to make it big. And we could then apply those patterns to our own businesses.

Marc Andreessen wrote a landmark article in 2007, on the only thing that matters. If you haven’t read it, go do so now. I’ll wait.

I re-read this article every few months. One line stood out to me the first time itself (and every time since).

He channels Andy Rachleff (Co-founder of Benchmark Fund, one of the most successful VCs) in his article, saying:

When a great team meets a lousy market, market wins. When a lousy team meets a great market, market wins. When a great team meets a great market, something special happens.

Thus, of the three key dimensions of a startup opportunity – market, product and team – market is far and away the most important aspect.

What’s the takeaway for an entrepreneur? Take aim at a humongous market, and put your head down and execute.

But is that true? Is targeting a large market the only important factor? Are the team, technology, etc. not as important?[1]

[fancy_box id=6][content_upgrade id=500]BONUS: Do you want this article as an easy-to-read PDF?[/content_upgrade][/fancy_box]

Is large market the most important factor?

It certainly is, according to the conventional wisdom. According to Andy Rachleff, again:

The best investments have high technical risk and low market risk. Market risk causes companies to fail. In other words, you want companies that are highly likely to succeed if they can really deliver what they say they will.

Don’t take market risk – i.e., aim for markets that are already large. Instead, take tech risk – where the product itself is hard to create.

This sounds great, and is a commonly accepted truism. And it also seems to be common sense.

But, again, is it true?

One way to settle this is to look at the performance of venture capital over time. As they say, nothing talks like money. But a quick look at VC returns can be quite sobering.

The Kauffman Foundation reports that VC hasn’t outperformed public markets since the late 1990s. In fact, since 1997, VCs have returned less cash to investors than they invested!

Could it be that this VC approach of taking high tech risk but low market risk isn’t working?

Tech matters (more)

I’ve just finished reading Crossing the Chasm, Geoffrey Moore’s landmark book. He presents technology adoption as a bell curve, with a few “gaps” between segments.

It’s easy to get the innovators and the early adopters. They want to be the first to try new technologies, so they’re primed to be convinced. You start hitting the main market only with the next group, the early majority.

Moore’s key insight is that it’s not natural to move from the innovators and the early adopters to the early majority. That’s why there’s such a huge chasm between these segments in the image above. A graveyard of companies that show great early traction, but suddenly hit a wall and collapse into the chasm.

His model suggests two pointers for technology companies:

Building a version of the tech, and serving innovators and early adopters, comes first.

The real challenge is crossing the chasm. You need to find a specific application to solve the early majority’s existing problems. This market isn’t visible or obvious at first – you need to create / discover it.

Thus, tech companies don’t take tech risk. They take market risk. If they find a big market, they succeed big. If they don’t, they fail.

Don’t take tech risk. Take market risk. If you find a big market, you succeed big. Else, you fail.

Jerry Neumann has written an excellent history of venture capital in the 80s. He makes a few similar observations (I paraphrase):

Whenever VC returns peaked, the driver was high market risk. Would there be a big market for computers (60s, Intel)? Would there be a big market for PCs (70s, Apple, Microsoft)? Would biotech become big (Genentech)? Would the Internet reach the masses, or would it remain a plaything of the elite (90s)?

These markets may seem inevitable today, but that’s just hindsight bias. Ask Ken Olsen. Or Thomas Watson. Or anyone in this article.

In most cases, investors didn’t take tech risk. Often, they found already-working products. Apple’s technology was already working when it raised funding.

Whenever VCs tried to reduce market risk to stabilize returns, they failed. For example, in the 80s, they entered more traditional, massive industries like retail. Result: returns were consistent and stable. But bad.

Thus, VCs didn’t often take tech risk. They preferred technologies that were already proven, and showed promise. And whenever they tried to reduce market risk by entering existing large markets, they failed.

At the end, Jerry summarizes:

The only thing VCs can control that will improve their outcomes is having enough guts to bet on markets that don’t yet exist. Everything else is noise.

There is no reason anyone would want a computer in their home – Ken Olsen, Founder, DEC

Peter Thiel’s Founders Fund adds its own voice to the argument. It highlights how, from the 60s to the 90s, VC was a predictor of the future. Today, though,

VC has ceased to be the funder of the future, and instead has become a funder of features, widgets, irrelevances. In large part, it also ceased making money, as the bottom half of venture produced flat to negative return for the past decade.

When you focus on incremental innovation, for a market that’s here and now, returns fall.

And last, Paul Graham makes a similar point, even more indirectly:

When something is described as a toy, that means it has everything an idea needs except being important. It’s cool; users love it; it just doesn’t matter. But if you’re living in the future and you build something cool that users love, it may matter more than outsiders think. Microcomputers seemed like toys when Apple and Microsoft started working on them… The Facebook was just a way for undergrads to stalk one another.

Build a product users love. Even if the market’s small today, it could become massive in the future.

I alluded to a similar point in a previous article, where I said that you must target a deep need for a narrow population, rather than a shallow need for a broad one.

[fancy_box id=5][content_upgrade id=430]BONUS: Get my checklist to identify bad startup ideas that sound good[/content_upgrade][/fancy_box]

What about the team, then?

As a VC friend of mine was quick to remind me when we discussed this, the quality of the team is incredibly important!

But this quality is not theoretical or bookish. It’s not about which Ivy League school you graduated from. Or even whether you have a string of successes under your belt (at least in consumer).

Instead, it’s about three things:

How driven you are. Will you overturn that 99th stone to find the gold mine? Or will the first 2-3 pivots fatigue you? Your initial ideas for tackling a problem will rarely be right. You’ll need to persist: find a new beachhead, and wade in again.

Are you willing to learn? Again, you won’t be right the first time. They say industry knowledge is a great unfair advantage. True, but it’s also a double-edged sword.

Can you execute?

So what’s the conclusion?

Which of these three is the most important?

The ex-consultant in me would answer, “all three”. And he’d throw in an “it depends” for good measure.

But it appears the conventional VC wisdom, of taking tech risk but not market risk, is wrong. As the Founders’ Fund article above says, the current trend of funding incremental innovations and more efficient solutions for existing markets is what has pushed VC returns downwards.

And what does this mean for entrepreneurs? Instead of trying to build something for large markets that VCs seem to be interested in, “swing for the fences”. But not in the conventional sense of aiming for large markets. Instead, try and piggy back on emerging trends that could become waves.

Sure, you’ll probably strike out. But should the market materialize, you will laugh all the way to buying the bank.

I’d love to hear your opinions. If you’re an entrepreneur or startup investor – what’s your stand on market risk vs. tech risk? Do email me at mail@jitha.me, tweet at @jithamithra, or comment here. I’d love to publish a follow-up sharing your opinions.

Thanks to Aditi Gupta and Abhishek Agarwal for commenting on drafts of this post.

[1] This article is about VC backable startup, and not a small business in general. Many great cashflow businesses (e.g., auto dealerships, general manufacturing) are often not high-growth businesses that can return 20x on invested capital, and are therefore not VC backable. See this article for a great description of such businesses.

Multi-sided business models are a unique phenomenon – unlike standard businesses which offer a product / service to a particular type of consumer, multi-sided businesses don’t offer any product / service. Rather, they provide a platform that connects buyers andsellers.

Think of Uber – it connects cab drivers and passengers, who benefit each other. E-commerce marketplaces are also examples – they connect buyers with sellers.

Such businesses face a natural chicken and egg problem. For the platform to be useful, both sides have to be present. Sellers won’t come on to your platform without buyers, and buyers won’t come either, unless there’s enough choice (i.e., sellers).

For example, people buy video game consoles only if there are games they can play. But game designers make games for a console only if there are enough people who own it. The proverbial chicken and egg problem. How do one solve this impasse?

The above article discussed a few ways in which businesses can break this deadlock. Many readers wrote in after the article, asking if I could create a framework / checklist that they could use to brainstorm ways to scale their own multi-sided businesses.

Towards that end, I recently published this presentation on SlideShare. Check it out, download it, and let me know what you think!

Regular readers of this blog and my newsletter (subscribe here if you haven’t!) know that I’m an avid reader. 2015, for me, was a year of quantity. I read 60+ books, and at least ten times as many articles.

Some of these were bad, some good, and some changed my perspective on work and life.

I could list the top 5 books I read in the year. But instead, let me present the top 5 ideas that transformed my thinking, and the books I found them in.

1. Keystone Habit – One Habit to Rule Them All (The Power of Habit)

I’ve written before about Thinking, Fast and Slow, and the difference between System 1 and System 2 thinking. The former is rapid, automatic, instinctive and judgmental. The latter is slower, more considered and analytical, and more effortful.

In most situations, we tend to use the quick-and-dirty System 1. The more methodical System 2 is quite lazy.

This proclivity to use System 1 underlines the importance of habits. Such sequential, repetitive tasks are so ingrained that we do them without thinking. The essence of System 1.

For instance, do you think when you’re brushing your teeth in the morning? More likely you’re so woozy you can’t walk straight. Still, your teeth are sparkling clean by the end of it.

That’s the power of habits – you can do certain tasks without thinking.

To understand more about habits, I read two books this year – Hooked and The Power of Habit. They talk a lot about the structure of habits, how to build good habits, how to break bad habits, etc.

But the most powerful concept to me was that of the keystone habit. Keystone habits are small, narrow habits in one area of your life that impact several other areas in a significant manner.

As Charles Duhigg says in The Power of Habit:

Some habits have the power to start a chain reaction, changing other habits as they move through an organization. Some habits, in other words, matter more than others in remaking businesses and lives. These are “keystone habits,” and they can influence how people work, eat, play, live, spend, and communicate. Keystone habits start a process that, over time, transforms everything.

A few examples of this are:

Exercise. When you start exercising, even if only once a week, it triggers changes in various other areas. You start eating better. You become more productive and confident at work. You show more patience towards your family and colleagues. All because of a few push-ups once a week. That’s a keystone habit.

Making your bed every morning. It’s a tiny, almost irrelevant change. But studies show that this correlates with better productivity, greater well-being, and more willpower.

Willpower. This is the most important keystone habit. Studies show that willpower in children is the most accurate indicator of academic performance throughout their student lives. Even more accurate than IQ.

At an organizational level as well, keystone habits can have transformative impact. The book cites an example of how a worker safety program at Alcoa ended up not only improving safety, but also turning Alcoa into a profit machine.

How do these small, unrelated habits have such widespread impact? In Duhigg’s own words:

Small wins fuel transformative changes by leveraging tiny advantages into patterns that convince people that bigger achievements are within reach.

So what are your keystone habits at life and work?

[fancy_box id=5][content_upgrade id=463]BONUS: Get my 2016 Reading List with 40+ book recommendations![/content_upgrade][/fancy_box]

2. Rewards and their Unintended Consequences (Drive)

Incentives are strange, powerful beasts. Whether it’s pocket money we give children for doing household tasks or bonuses our bosses give us for exceeding sales targets, incentives play a key role in driving us to perform.

I think I’ve been in the top five percent of my age cohort almost all my adult life in understanding the power of incentives, and yet I’ve always underestimated that power. Never a year passes but I get some surprise that pushes a little further my appreciation of incentive superpower.

Given the immense power of incentives, it becomes all the more important to design them right. If they’re even slightly misaligned, they can “damage civilization” (Munger’s words, a tad hyperbolic).

I read Drive earlier this year – an insightful book on the powers of rewards. The book also talks about the negative influences of incentives, if not designed well.

Incentives can drown out intrinsic motivation, even when you’re doing a task you enjoy. If you receive an incentive for doing something, you also receive a subliminal message that the task is not worth doing without the incentive. End result: incentives transform an interesting task into a drudge, and play into work.

[Tweet “Incentives transform an interesting task into a drudge, and play into work.”]

Incentives can only give a short-term boost. Like caffeine, they’re useful when a deadline looms. But beware the energy crash that will inevitably follow.

Rewards can become addictive. As Daniel Pink, the author, says – Yes, rewards motivate people. To get more rewards.

Incentives do have their uses, but only for process-oriented tasks. In fact, incentives for creative tasks can impede progress. They narrow your focus at the exact moment when you need broad thinking.

The book captures many more interesting and significant implications of an innocuous, innocent incentive.

3. Your MVP can be more “minimum” than you think (Lean Startup)

Most people working in the startup ecosystem are familiar with the Minimum Viable Product. The MVP is the most basic version of your product that still delivers your core offering.

It’s an important concept to keep in mind as you build a product. You don’t want to spend too much time building the first version, before realizing customers don’t want it.

I thought I’d understood the concept well. I congratulated myself as I built my first product in three months, found that people didn’t need it, and junked it. And again when I built my next product in four months, tested it with customers for three, and then pivoted it to its current form.

Then I read Lean Startup.

I realized then that I’d taken far too long to build my MVP. What’s more – so had everyone else I know. Why do we all take so damn long to build an MVP?

The reason is that we’ve got the concept wrong. You don’t need to ‘build’ an MVP. You just need to put it together.

What does that mean?

Let’s say you want to create a website offering fashion tips. You can launch in one day or less.

Buy a domain. 3 hours (the actual purchase will take 2 min. But I know you’ll agonize over names for the remaining 2 hours 58. And no, the name won’t matter.)

Build a landing page with Unbounce where people can ask questions or upload photos. 1 hour.

Run a small Facebook campaign publicizing the site. Or tell 10 friends, and tell them to tell 10 more each. That’s your test audience. 2 hours.

Thus, you can be up and running tomorrow! Even if you’re slow because this is your first time.

[Tweet “Your Minimum Viable Product can be more “minimum” than you think.”]

Many popular products of today hacked together such makeshift MVPs when they started. Check out the article in Further Reading for examples.

4. Pareto Principle & the Minimum Effective Dose (Four Hour Work Week)

Four Hour Work Week, by Tim Ferriss, is THE book to read on personal and business productivity. Unlike most productivity books and blogs, he eschews all the standard life-hacking methods (of the “shake your hips while you brush your teeth, to get some exercise” variety).

All he has to say about traditional time management is, “Forget all about it.”

[Tweet “All you need to know about traditional time management is, “Forget all about it.””]

Instead, he focuses on using the Pareto Principle, or the 80/20 rule. He uses this to introduce the concept of the Minimum Effective Dose – the smallest amount of effort for the most impact.

Whether your customers, your vendors, books you read, anything – choose the few that give you the most value, and forget about the rest.

He should know. He puts the Pareto principle on steroids. Sample this:

In his nutrition products business, he “fired” the least profitable 97% (!) of his customers, to instead focus on the 3% most promising ones and double his income.

He eliminated 70% of his advertising costs and almost doubled his direct sales income.

He discontinued over 99% of his online affiliates.

Eliminating the least value tasks and business relationships helped him free up his time to do more productive tasks. And achieve the Holy Grail of less work but more profit. That’s how you do productivity!

Side note: In his follow up book, The Four Hour Body, Ferriss uses the concept of the Minimum Effective Dose to illustrate how to become more healthy. Check that out too.

One skill I tried to build last year was negotiation and persuasion. I read three great books on the subject. I’m still to have the investor conversations where I’ll use this skill, so I don’t know how much they’ve helped!

But one concept that has stuck is that of the BATNA – the Best Alternative To a Negotiated Agreement. In simple terms, the BATNA is your fall-back option in case talks fall through.

Your BATNA is tantamount to your leverage in the negotiation. It works in two ways.

1. The better your BATNA, the more leverage you have.

Let’s say you’re negotiating the sale of your house with a prospective buyer. Your alternative to this is to (a) rent it out; (b) sell it to a land developer to make a parking lot, and (c) live there yourself. If option (b), say, is the most attractive of these, then that’s your BATNA. The value the land developer offers you should form the baseline for the negotiation.

As long as the buyer’s offer is higher than this, you can reduce your price (after making a big deal of it, of course).

Far more important though, is that if the buyer pushes you below this BATNA, you can and should refuse. This is difficult. We tend to over-invest emotionally in a long negotiation. But with this hard stop in mind, you can overrule your emotions and walk away.

2. The worse you make your opponent’s BATNA, the more leverage you have.

Improving your BATNA gives you leverage. Straightforward. But there’s a more interesting insight here. You can improve your leverage by worsening your opponent’s BATNA.

Let’s say you’re the prospective buyer in the above transaction. You know that your seller is holding out because of the safety net of the land developer.

So, you remove that safety net. For example, you could sell one of your own other properties to the land developer, so he’s no longer making an offer to your seller.

By removing the most promising alternative your seller has, you’re weakening his leverage. And strengthening your own considerably.

[Tweet “Show your opponent he has a lot to lose from breaking talks, and he’ll be surprisingly pliable.”]

6. [BONUS] Focus on strengths, not lack of weaknesses (The Hard Thing about Hard Things)

By default, we are all risk averse. In fact, Loss Aversion is one of the strongest, most deep-rooted cognitive biases there is, squirming deep inside our brain’s reptilian core.

This loss aversion manifests itself in several ways. Holding on to bad-performing stocks in the hope of a turnaround. Not making bets because of high risk, even if the reward is much higher.

In the corporate environment, this results in a preference for well-rounded candidates. We tend to choose such people over others who are spiky in some areas, but middling in others. We choose average programmers with great communication skills over 10x programmers who are introverts. We reject uber-salesmen just because they don’t know much about tech.

As Ben Horowitz says in this book, that’s the exact wrong approach. That’s not how great organizations work. Instead, such organizations look for excellent candidates, who are in the top 1 percentile of their roles. Never mind that they’re not good at other things.

“Identify the strengths you want, and the weaknesses you’re willing to tolerate.”

Your Product team should have the best programmers. Even if their communication skills could be better. For sales, hire the best salesmen out there, even if they’ve not worked in your industry before.

We also tend to paper over the weaknesses and focus on repairing them. Again, not the most optimal approach. Instead, focus on honing your employees’ strengths. Plug the weaknesses (If they’re important. They often aren’t.) by hiring superstars in those areas.

[Tweet “Identify the strengths you want, and the weaknesses you’re willing to tolerate.”]

[fancy_box id=5][content_upgrade id=463]BONUS: Get my 2016 Reading List with 40+ book recommendations![/content_upgrade][/fancy_box]

So, those were the books and ideas that captivated my thinking in the last year. Here’s to many more brilliant ideas and books in the new year. Of course, you’ll be the first to know of any great books I find (sign up here to receive regular updates!).

A few weeks ago, my wife and I were in Galle, Sri Lanka for a much-awaited vacation. We chose a villa with great reviews on TripAdvisor. It seemed a decent place. A little far from the main town, but the hosts were quite friendly.

But we couldn’t get much sleep any of the nights we stayed there, because our room had bedbugs.

After we came back from the trip, we made sure to rate the place. We left not one, but two ratings (one each from my wife and me). Both of them were 5 stars.

Wait, what?

Did we enjoy getting bitten by bedbugs?

I was surprised too. Not just at my own rating, but at other ratings on TripAdvisor too. This place was one of the most recommended ones in Galle!

So how did this happen? How did I – and all the other guests – rate inferior customer service so highly?

Do ratings work?

The prevailing wisdom is that ratings work. That’s why they are everywhere. When you open an app on your Android phone, it asks you to rate it on the Play Store. Complete a ride on Uber, and you have to rate your driver. Order something from Amazon, same story. Open your inbox after a long vacation, and what’s the first email you see? A message from either your airline or hotel, requesting you to rate your experience.

I’ve always found the act of rating quite empowering. The equation is simple – if you can rate a service provider in public, he has every incentive to ensure that you get great service. Right?

Well, after that incident in Galle, I realized that ratings may not result in better customer service. In some situations,they may be worsening it.

Wait, how does that make sense?

I’ll explain. But first, let’s agree on two key facts about ratings.

1.Ratings have an impact on service providers.That’s one reason they’re ubiquitous. Drivers on Uber do get blacklisted for low ratings. Top-rated hotels on TripAdvisor do get ten times as many bookings as lower-rated ones.

2.Customers know ratings have an impact.This makes them capricious (this Verge article calls them – us – entitled jerks). To see this, you only need to see a few app reviews. Sample these ratings on Circa (an app that used to provide summaries of important news):

Ratings are supposed to highlight how good an app is. But no, sometimes you get a 1-star for an innocuous review request.

This customer fickleness is not just an app store phenomenon. As the Verge article says,

We rate for the routes drivers take, for price fluctuations beyond their control, for slow traffic, for refusing to speed, for talking too much or too little, for failing to perform large tasks unrealistically quickly, for the food being cold when they delivered it, for telling us that, No, we can’t bring beer in the car and put our friend in the trunk — really, for any reason at all, including subconscious biases about race or gender.

Please the customer, and hope for the best

The fact that we wield a strange amount of power and know it, turns upstanding, proud cab drivers and B&B hosts into fawning, obsequious and servile slaves. You can’t jilt or offend a customer in any way. A single misstep, and you get a 1-star rating. Not a 4- or 3-star. Your last five customers may have given you 5 stars, but this single rating could put you out of business. In New York, Uber delists drivers from the platform if they go below a 4.5 star average!

So what is a service provider to do? Provide honest-to-God great service.And hope that nothing gets screwed up.

But there’s an easier way.

The honest approach is hard, time-intensive and expensive. And it’s subject to random whims of the entitled customer.If a customer expects Hilton service at McDonald’s rates, you’re bound to get 1 star.No matter what you do.

But there is an easier, quicker and more inexpensive way. One of the oldest psychological tricks in the book.

Dr. Cialdini, the author ofInfluence, calls this trick “Liking – The Friendly Thief”. Studies show that if you spend more time with a person, you end up liking her. And if you like a person, you tend to favor her in your dealings.

At a certain level, this is obvious. But that doesn’t make it any less powerful. Malcolm Gladwell cites a great example of this in Blink. Patients don’t file lawsuits when they suffer shoddy medical care, if the doctor is polite. They only file when they feel the doctor mistreated or ignored them.

“People just don’t sue doctors they like.”

So, to get a great rating, all you need to do is: (a) smile a lot and appear likeable; and (b) talk a lot, to create a human connection and familiarity.

Tried and tested. Once you get to know the service provider, you’d be a stone-hearted reviewer to leave anything less than 5 stars.

Nice host + bad customer service = 5 star rating

That’s what happened to us in Galle. Even though I was aware of this cognitive bias, I was powerless to counteract it.

The owner received us with great cheer. He chatted with us for hours. Always smiling and laughing (even when I didn’t crack a joke. And I’m not that funny anyway). I learned a lot about his life. I commiserated on his past troubles, and lauded him on his recent turn in fortunes.

My room still had bedbugs.

But my wife and I didn’t complain. Who can tell off such a nice guy? And when he requested us to leave two ratings on TripAdvisor, how could we refuse?

Talk more. Do less. Get 5 stars. Repeat.

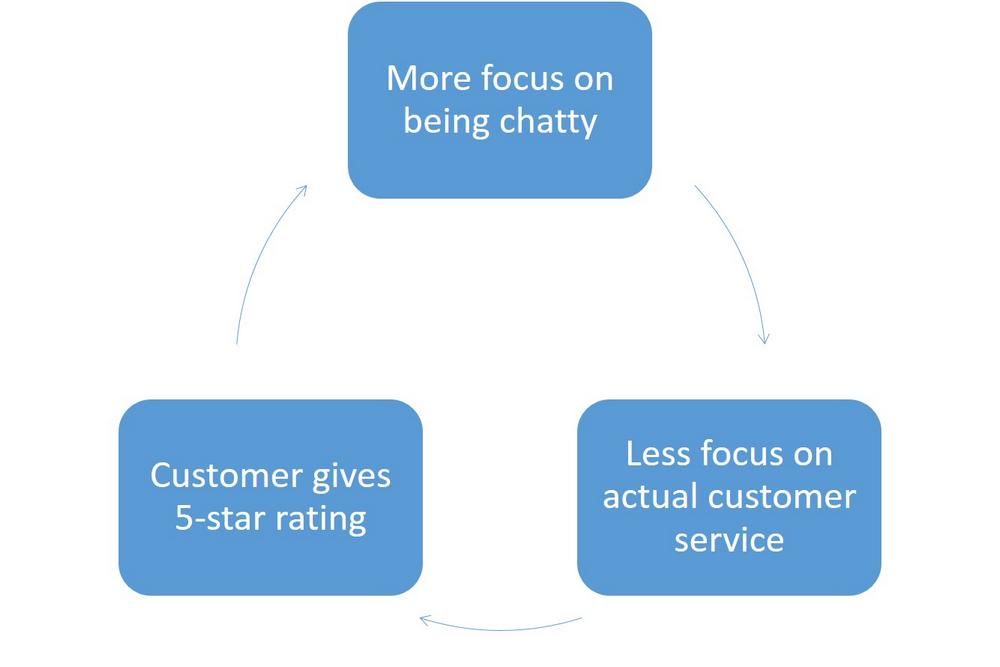

This is just one small episode. But it sets in motion an insidious feedback loop, which could result in worsening customer service over time.

Customer give a 5-star rating despite bad customer service.

Service provider sees this as validation of his strategy. And becomes more chatty, more fawning.

Soon, if he’s smart (our guy was), he realizes there’s no return on actual customer service. It’s much easier to smile and bluster, than it is to clean the room. Over time, he’ll become more talkative, and truecustomer service will degrade.

Woe betide the unsuspecting traveler when that happens.

Thus, ratings may have an impact that’s thepolar opposite of your intention.

How do we break this loop?

Now, I’m sure you want great customer service. So, how can we break this loop?

Just being aware of what’s happening is not enough. You’ll only feel worse, as you continue to give 5-star ratings like a powerless lab rat.

The only way to break this cycle is to have a system of multiple ratings on different attributes, instead of one single unidimensional one.

Why would that work? For three reasons:

It would force objectivity.If you’re rating your stay at a B&B separately on Cleanliness, Quality of Food and Friendliness of Staff, you’re more likely to question the halo around your host’s head, and distill your cheery feeling into its components

It would give the service provider the right feedback on how to improve.

Ratings are here to stay. Let’s make sure they actually improve customer service. Rather than slowly turning us into smiling zombies.

The startup bug has bitten you. You want to start a business, grow it for a few years, sell out and rest easy for the rest of your life. A great dream to have. But that’s the easy part. The hard part is building the business. And this long, arduous journey starts with a single step – having a great idea.

How do you come up with a startup idea? To start, you read this article by Paul Graham of Y-Combinator. It’s thought-provoking, even by Paul’s lofty standards. Paul says a lot about the characteristics of great ideas. But he also talks about a similar-looking but antithetical concept – the “sitcom” startup idea.

What is a sitcom startup idea? It’s one which sounds plausible, but is actually bad.

This is not just a bad idea. We have tons of those, and they are easy to identify. Even if our ownership of the idea blinds us to its infantile stupidity, our friends will warn us. They’ll tell us it’s the dumbest thing they’ve ever heard. And we can swallow our pride and move on to the next idea.

No, the sitcom startup idea is not bad in the same way. It’s an idea which sounds plausible. So plausible that when you go ask customers whether they’d use it, they don’t say no.

This is what makes it dangerous. You can read Lean Startup, dutifully ‘validate’ your idea with customers, and then build it. Only to find out that there actually is no market.

Social network for pets

Paul illustrates this with an example of a ‘social network for pets’. If you have pets, this sounds like a good idea. Sure, you can imagine posting photos of your pet parakeet on petlife.com, where others are waiting with bated breath to “like” them. Or, what’s far more insidious, you can imagine others around you loving this service.

I actually tried this during my lecture in IIM Trichy, and people loved the idea. But it’s bad on two levels:

It’s erroneous to assume that if people say they like a product, they’ll use it. I might like 30 different websites, but that doesn’t mean I’ll check all of them every day. Given my limited attention span, the only social network I’ll use daily is Facebook.

If you talk to 100 people and they all say they “know someone who would use this”, then you’ve found yourself a community of 100 almost-users. Or to be precise, exactly zero users.

So how do you differentiate between sitcom startup ideas, and truly promising ones? How do you know if you’re on to something huge, or just a mirage?

The short (and hard) answer is – you try anyway. You build an MVP and check if there’s traction in the market. If there is, congratulations, it worked. If there isn’t, then you know you just had a “sitcom” idea.

But there is an easier way. I’ve come up with a few patterns to identify what is probably a bad idea, even though it sounds plausible.

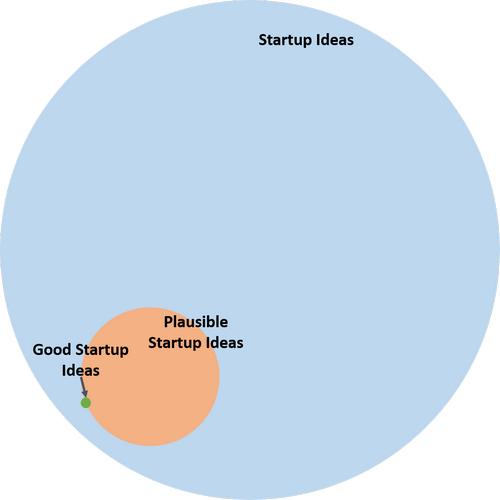

Before we jump in, a caveat. I don’t know if any plausible sounding idea is actually bad. What I do know though, is that the universe of plausible ideas is much, much larger than the set of good ideas. So, an idea that is only plausible is probably bad.

Just like I know that a monkey banging away at a keyboard will not produce Romeo and Juliet (it might, but the probability is infinitesimal), if all I know about a startup idea is that it’s plausible, it’s probably bad. Sure, you get a Twitter every once in a while. A product that seems random can suddenly catch fire. But such instances are so few and far between that you can ignore them.

With that done, let’s dive in to the patterns:

1. Broad and shallow, vs. narrow and deep

One of Paul’s theses in his article is that you should solve a deep need for at least a few people. If the need you are solving is shallow, then it’s not a great startup idea. Even if it affects a broad set of customers.

It’s got to be a major problem – a mild or one-time issue won’t cut it.

You’ve got to create a product that at least a few people NEED, not one that many people WANT.

A sitcom idea of the ‘broad and shallow’ variety can follow several patterns.

A “vitamin”, not a “painkiller”

The social network for pets falls into this category. It’s a nice-to-have, like a vitamin capsule. No one needs it, like the root-canal patient who’ll pass out without a painkiller. If people just ‘want’ what you’re building but don’t ‘need’ it, tread with caution. You may be onto a bad idea that sounds good.

Instead of focusing on cool things people could use, try and solve a real problem.

Not solving a top-tier problem

But only solving a problem is not enough. It has to be important. Simply put – if the problem you’re solving is not one of your customer’s top 3 problems, it’s not important. Give up now, before it’s too late.

I once thought of building a software tool to help VCs manage deal flow. It would have a visual funnel, to tell the VC how many deals they have seen in the last 3 months, and at what stage of discussion each deal is. And they could dice it by any filter (e.g., SaaS vs. consumer, location, stage of business, etc.) to see their deal pipelines.

A great idea, I thought. The only issue – it’s not an important enough problem. Getting strong deal flow is far, far more important than tracking it. Many VCs are happy enough using Excel to track their pipelines. They’re not even trying generic funnel management systems like Salesforce. Why will they bother using one tailored for VCs?

If the problem you’re solving is not one of your customer’s top 3 problems, it’s not important.

“Solving a problem people don’t know they have”

This is a first cousin of the two patterns above. While not a “vitamin” solution per se, it’s solving a problem people don’t know they have. Which begs the question – how do you know they have this problem?

I tried doing this a couple of years ago, with a plug-and-play loyalty program for small business websites. Users would get points for coming back to the website every day, reading articles, sharing to social networks, etc.

A great idea for large, stable businesses trying to increase customer retention, maybe. But a small business finding its feet? These guys don’t even think about gamification or loyalty. They have other problems. They need to build a user base first, before trying small tricks to engineer loyalty.

I tried selling this for 6 months. It did not work. It’s hard enough convincing people to buy your product. Why do you want to add the burden of convincing them that they need it?

If you want to avoid building something no one wants, then solve known problems.

“This product solves everyone’s problems” OR the “Microsoft Office” product

I love Microsoft Office. It’s so flexible, so all-encompassing. No matter what type of problem you’re working on, you can bet that Excel and PowerPoint will be super helpful. Or think of Google – no matter your query, you can find the answer.

These are all excellent products. But aiming to solve everyone’s problems in one go can sound the death knell for startups. Why? Taking the example of my gamification system again:

It’s unlikely that there’s a dire need for your product among a huge mass of people already. If you’re solving a problem for everyone, it’s probably a broad and shallow problem, not a deep one. My system was a nice-to-have, not the answer to their top 3 problems.

In most cases, flexible products necessitate a learning curve among customers. Newsflash – your customers are too busy to spare any time to learn how to use yet another product. Unless you’re solving a problem as critical as the ones Office and Google solve, good luck getting adoption. It’s more sensible to focus on one type of customer, and solve their problem better than anyone else.

Solving everyone’s problems at the same time requires a complex back-end. Why build that without strong market validation first? You’ll either end up building a buggy product, or worse, build a great product that no one wants. In the case of our product, the tech challenges proved intractable. Trying to integrate our system with several website technologies meant that it didn’t work well with any.

Trying to solve a problem for everyone often means you end up solving it for… no one.

“Cool product I’ve built”

You get this a lot from engineers (I’m one too). We focus on the product, because we feel that the product alone is good enough. “My cool new app allows you to share your photos with all your Whatsapp groups in one go”. Great, but what if your users don’t want that?

“Build it and they will come” doesn’t work, in this world where a million apps are fighting for people’s eyeballs. See the chart in this article to see how high the bar is. You need to be sure that you’re solving a problem, and a top-tier one. Else, you could just be a “solution searching for a problem”.

Demonstrate need first. Else, your intricate product could just be another elaborately constructed pipe dream.

2. Templatized business models

“Uber for X”

[as used in “Uber for bicycles: On-demand bicycles for your riding pleasure”, or “AirBnb for cars: Rent other people’s cars when they’re not using them”]

“Do you want a bicycle at this very moment?”

This template is as old as the Internet. Take what’s working in one sector, and plonk it into another. It was “Website for X” in the 90s, and “Social network for Y” in the 2000s. But it’s a dangerous stratagem. Why?

Sure, Uber has been uber-successful in the cab market. But that doesn’t mean on-demand could work for every other sector. Unless the idea has grown organically from a problem, you have to assume it’s bad. You have to assume that the founder has applied the Uber template to the first sector he could think of.

Another clue that you’re facing this situation is when founders have no real expertise in the area they’re building for. Then how do they know that the problem is real? They don’t. All they know is that the solution is real, for another sector.

“X for India”

This is an even more pervasive and notorious template. Unless the model has some kind of geographical constraint (e.g., on-demand cabs), there’s nothing stopping a successful US business from expanding to India.

Moreover, if the model involves network effects, then you’d expect something that’s grown in one place to capture share rapidly in other places too.

As Mahesh Murthy is wont to say, the Facebook of India is Facebook. The Tinder of India is Tinder, and not Woo.

There’s one more problem with this template – some models just don’t extend across geographies. On-demand bicycles may be a great idea in Scandinavia or Taiwan. But it just won’t work in hot, sultry, noisy and overcrowded Mumbai (gosh, why am I still living here?).

3. Incremental business models

This is another type of business idea that we see quite often. It often involves just a slight tweak to solutions existing in the market. Again, this can be of two types:

Cloning an existing player, but with slight improvement

Think “Uber with wi-fi”. Of course, Uber has started doing this now. But even if it didn’t, this would be a horrible idea for a startup. Wi-fi is not differentiation. It’s a cosmetic touch-up engineered solely to help you raise money from rookie investors.

It’s wrong on two levels:

It assumes that the incumbent will sit idle while you bring out an improved product. If what you’re bringing to the table is only an incremental improvement (i.e., 1x, not 10x), you can bet that the incumbent will also include it in their next release, if they find out it’s a helpful add-on. Don’t assume stupidity.

Often, your improvement has nothing to do with the core problem you’re solving. Wouldn’t it be silly to say, “Uber works, but people hate the fact that it doesn’t have wi-fi.”?

Cloning an existing player, but in an adjacent market

Back when Bookmyshow (a movie ticketing website in India) was only a couple of years old, a friend told me he wanted to build a “Bookmyshow for Plays”. This is a bad idea too. Bookmyshow had already solved the harder problem of getting customers. So, it was much easier for Bookmyshow to include plays on its platform, than it was for a new player to start afresh. And true enough, plays appeared on Bookmyshow a few months later.

A giveaway for this kind of sitcom idea is a statement of the form “Today’s solution is satisfactory. But mine’s much better”. For your idea to be definitively good, today’s solution cannot be satisfactory! At least for a segment of the audience. Otherwise, your idea would be like my deal flow management solution for VCs. A nice-to-have, but not nice enough to change an existing process.

What is nice enough though, to change one’s existing behavior? A 10x improvement – whether in ease, time taken, or effectiveness.

4. “No Competition”

You often hear founders say that they’re the first team to do X, and that there are no competitors. Or they may say that everyone is a competitor (which is another way of saying “no competitors”). If you hear this, run in the opposite direction as fast as you can.

Why? Why is lack of competition alarming? For two reasons:

If there really is no competition, maybe the market itself is unattractive. Today, it is difficult to come across a problem that no one has seen at all. Why do you want to solve unambitious problems, when it’s just as difficult as tackling ambitious ones?

The founders may not have done thorough analysis, or may be suspended in the myth that their competitive moat is bigger than it actually is. Would you want to back such founders?

Wait, so am I saying competition is actually important? Yes – many players trying to solve a problem demonstrates strong need. But to succeed, you still need to differentiate. You need to have an ‘unfair advantage’ in startup parlance. Whether industry experience, critical partnerships, etc. – you must have a secret sauce in your recipe for success.

Your competitors will not sit idle while you beat them. What’s your secret sauce?