Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the ultimate-blocks domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /var/www/wp-includes/functions.php on line 6121 books Archives - So it Goes.

Successful entrepreneurs, investors and strategy experts all extol the virtues of focus. I have as well, as a strategy consultant, then a founder, a writer, and now as a seed stage investor at OperatorVC.

“If you focus on a small segment, you can own it, dominate it.”

So the conventional wisdom goes.

But there are times when focus can constrain a startup from achieving its potential. When you become a big fish in a small pond, while there are gloriously large oceans just around the corner.

How do you know which is which? How do you know when to focus, and when to extend?

This came up in a conversation with Ankesh Kothari, a fellow entrepreneur and seed investor. He highlighted how a lot of startups focus too narrowly on a small market, and never expand. And we often see the opposite at OperatorVC. Startups trying to solve problems across a broad swathe of consumers from the outset. “Microsoft Office products that solve everyone’s problems”, as I call them here.

Here’s what’s interesting: neither of these is always the right answer.

Sometimes, you have to focus on a specific consumer segment. Make sure you solve a need deeply. At other times, you need to expand your horizons.

If you focus too acutely, you’ll never become a $100 million company.

This is not intuitive. You can’t be deep in the weeds one moment, and flying at 20,000 feet the next.

Great founders can alternate between these two opposite behaviors well. And legendary founders plan for this in advance.

Before Tesla started, Musk anticipated when he would focus. And when he would extend lower in the price pyramid. And he wrote it all in a badass blog post, for all the world to see.

[Tweet “If you focus too acutely, you’ll never become a $100 million company.”]

So how can you be more like Elon Musk?

At its very basic, it’s three simple steps:

Start with extreme focus. Focus on a narrow segment. Serve that segment’s needs so completely that you build a monopoly in it. Focus on a city, community, or neighborhood, and then OWN it

Then, expand into an adjacent segment

Repeat steps 1 and 2.

Several great startup successes have done exactly this:

Facebook: Started with a student listing, just for Harvard. Once Zuckerberg found product-market fit there, he then expanded to other universities. And then the rest of the world.

Uber: Started as a premium limo service. Only for select customers, only in San Francisco. Today, there’s a good chance you’re reading this sitting in an Uber.

In the 70s, two Harvard geeks built a simple Basic interpreter for the Altair, a decidedly non-popular microcomputer. How would that ever grow big? It did. You might have heard of Microsoft.

Now, I know what you’re saying. Hindsight is 20:20.

Is this just one of those clichés that you retrofit to success stories? Or is there actually a lesson here for people just starting out?

Is it even possible to be more like Elon Musk?

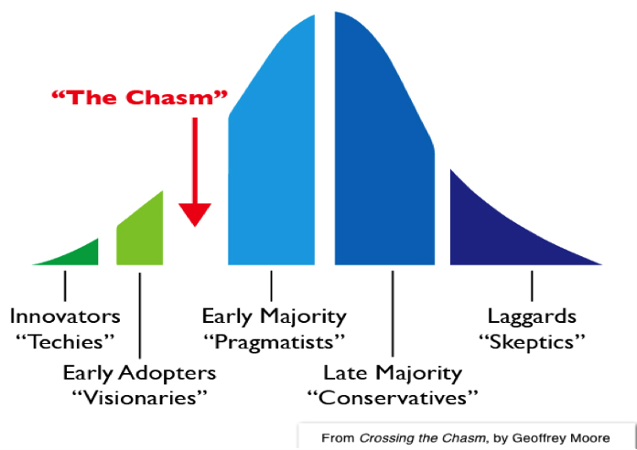

The Chasm model of product adoption is a great framework to know when to focus, and when to extend.

At the trivial level, we all know this. Tech enthusiasts and early adopters will use your product first. The mass market (the Early Majority or “Pragmatists”) will gradually start using it later.

But the Chasm Model offers two new insights:

There’s a “chasm” between the early adopters and the mass market (the early majority). It’s very hard to make that leap, and many startups die trying.

Unlike the early adopters, the early majority aren’t interested in your tech. They are interested in its application to their most important needs.

And therein lies the way.

When to focus

Focus when you’re crossing the chasm.

Focus on a single narrow niche within the mass market. Understand that niche and its most important needs. Create an application of your technology tailored to that segment’s needs. Find product-market fit, and cement your place there. Own that niche.

Let’s take an example we’ve seen at OperatorVC. Say you’re building an AI based system to help people recover from illnesses. Don’t start coding algorithms for all the million diseases that are possible. Don’t even start with the 100 most prevalent diseases. Start with one disease. Just ONE.

When to extend

Extend once you own that first segment.

Select the next niche(s) in the mass market that you want to own. Again, design applications of your technology for those segments.

And REPEAT.

This is exactly what Tesla is doing now, working its way down the price segments.

Once the healthcare bot is perfect for that one disease, it’ll be much easier to expand to the next disease. And the next hundred.

[Tweet “Be like Elon Musk. Focus first. And then extend to own the world.”]

So, when you’re starting off, make sure you focus on a segment you can really own. But also be ready to extend later, so you can own the market.

One year ago, I started the Sunday Reads newsletter. It’s a short email that goes out once every week (on Sunday, obviously), with “the best articles on business, strategy, entrepreneurship, and everything in between.”

Every week, I share the best articles I read that week. Sometimes they’re organized around a theme. Sometimes not. But there they are, without fail, in your inbox every Sunday.

I realized just last week that over the year, I had shared 600+ articles through that weekly email. And often, I read at least ten times as many articles during the week, to choose these best 10-12 articles.

What have I learned from these 6,000+ articles? Have they made me better at what I do?

No trees were harmed in the making of this post

A part of me answers almost immediately – yes, for sure! But how exactly have they helped? Can I tease out the key lessons I’ve learned from the articles? Or is it just a vague sense of achievement and hope – surely I haven’t wasted those hours?

So, over the last 7 days, I went back to those 52 emails. And pulled out the key learnings and principles that I’ve actually tried to use in my life.

Two caveats before we go on:

First, this is a long post. I’ve tried to summarize the key concepts I’ve learned, and it turns out 6,000 articles means a ton of learnings!

Second, I’ve included (several) links for further reading. Every paragraph is a rabbit hole. So, first read through the whole thing without clicking through on any link. Then, come back. Feel free to dive as deep as you want, on the subjects that interest you.

1. Goals don’t work. Use systems instead.

This was not a new lesson for me. But across article after article, book after book, this got reinforced. No matter the field, what seems to work is understanding the basic principles and following them. That’s it.

Success is not about choosing an ambitious goal and stretching to reach it. Whether in running your business or trying to win arguments with your spouse, hard work won’t cut it. Instead, you understand the basics, try a lot of different things, learn what works, and iterate or double down.

If you do it right, then no matter whether you succeed or fail in one specific endeavor, you’ll always come out ahead. You’ll always learn something that’ll be useful next time.

[Tweet “Goals are for losers. Use systems instead.”]

This sounds a little hackneyed at this high level, I know. But as you’ll see, it permeates all the other lessons below.

Further reading:Goals vs. Systems. I’ve read this a few times before, but I was still blown away by the simplicity when I read it just now. If you like this, you’ll love Scott Adams’ book.

2. Growth Mindset vs. Fixed Mindset

There are two types of people – those with a fixed mindset, and those with a growth mindset.

If you have a fixed mindset, you think you are at the peak of your skills. You’re the best artist, manager, husband, wife, etc. you can be.

If, on the other hand, you have a growth mindset, then you strongly believe you can grow and improve at whatever you do. Whether in your personal life (you can always become a better husband. OK, that hit too close to home), or in your professional career. There’s always room for improvement.

Your mindset determines how successful you are to a surprising extent. People with growth mindsets are more willing to try new things, learn new skills, and take risks. And those who take risks, get the rewards. Fortune favors the brave, etc.

Further Reading: You can read Carol Dweck’s book Mindset, which outlines the research on the subject. Or read Maria Popova’s review of the book.

3. Deliberate Practice

Let’s say you have a growth mindset. Is that enough to grow and improve your skills over time?

If the goals vs. systems argument tells us anything, it’s that just believing you can improve at something isn’t enough. So, what’s the system for this?

Practice. Not just doing something for 10,000 hours. Deliberate practice. Working at the edge of your abilities, getting immediate feedback (succeeding / failing), learning, and trying again. That’s what builds skills.

If you want to learn business, start a side-business. At every stage – idea generation, building your first product, selling it to your first customer – you’ll fail the first few times. And you’ll learn immensely.

If you want to improve your writing skills, start a blog. It takes 2 minutes on Medium. Write every day, and ask your friends and colleagues for feedback. Rinse, repeat.

[Tweet “Don’t just practice. Do deliberate practice. That’s how you build skills.”]

Further Reading: Cal Newport’s book on the subject is excellent. This article from his blog is a good summary of the six traits of deliberate practice.

These were the three most important learnings for me from my last year of reading.

Take a systems approach to all your endeavors

There’s always room to become better at what you do

The “system” to become better is deliberate practice

Everything else stems from these key principles. They form the foundation for the rest of the learnings. Get these right, and everything else falls into place. How’s that for a system?

As I continued plowing through the articles, I saw that a lot of them were organized around skills essential to succeed in the workplace today. Communication, structured thinking and problem solving, creativity, and focus (especially focus), to name a few.

How do we build these skills?

4. How to learn anything

Communication, structured thinking, etc. are critical skills. But there’s one skill that’s a precursor to all this – the ability to pick up new skills quickly.

As Scott Adams says in his book, every new skill you learn doubles your chances of success. To take a simple example – an MBA who knows to code is far more valuable than just an MBA. And if this person also understands, say, cinematography, then the unique opportunities available are far more lucrative.

So, you need to continually build new skills throughout your career, to take advantage of new opportunities. And ideally, you’ll build skills that are themselves useful across a diverse set of sectors (system approach again).

[Tweet “Every new skill you learn doubles your chances of success”]

OK, you’re sold. Learning how to learn is key (it’s also the secret moral of Kung Fu Panda, but that’s another story).

But how do you learn? You could join a course at your local university, or hire a teacher online, and do your 10,000 hours.

Or, you could use the Pareto principle to identify the 20% of concepts that have 80% of the importance, and quickly learn and practice those.

Don’t you want to be that guy, who always sees through to the crux of an issue? Who understands the real problem, which no one else can see? Who always sees the way out of an unresolvable predicament?

I certainly want to be that guy.

Turns out, this is a learnable skill.

a. Don’t be stupid

Charlie Munger, Warren Buffett’s partner-in-crime, once said, “The best way to be smart is to not be stupid”.

We are not rational beings, as economists would have us believe. Not by a long shot. As I’ve written before, we’re not only not rational, we’re also irrational in consistent and repeatable ways.

We’re subject to several cognitive biases, which predictably warp our judgement.

Anchoring is one example of a pervasive bias. The first number thrown in a negotiation becomes an unconscious anchor to the rest of the bargaining. That’s why both parties fight to shout out the first bid.

Availability bias is another one. We overestimate the probability of an event if we can remember vivid instances of it. We pay more for earthquake insurance than for calamity insurance (even though the latter includes earthquakes!), we overestimate the possibility of winning the lottery if our neighbor just won it last week, and so on.

How do you avoid these biases? Here’s the thing – you can’t.

Since these operate at a subliminal level, just knowing them won’t prevent them. Next time someone makes the first offer in a negotiation, you’ll predictably bargain around that.

Instead, counteract these in your decision-making by using a two-track thinking process.

First, make a decision rationally (to the best of your abilities)

Then, try and recognize the biases you’re subject to, and adjust accordingly

Do this again and again, and you’ll soon become a natural. At not being stupid.

[Tweet ““The best way to be smart is to not be stupid””]

b. Develop a latticework of mental models

This idea also comes from Charlie Munger.

There are several different frameworks that help us understand the world. Understanding and building a repository of these frameworks in our heads can help us become much faster at comprehending the forces at play around us.

Whenever you read anything interesting or insightful, or see a surprising pattern, put it down in a notebook.

Over time, this will become a repository of the smartest things you’ve read. A surprisingly easy place to go back to whenever you need inspiration, or a way out of a thorny problem.

[Aside: if you want to learn how to have great startup ideas, read this guide. But be warned, you’ll sometimes come up with ideas that seem to have a lot of potential, but are actually bad. Here’s how to recognize bad ideas that look good.]

7. How to communicate better

a. How to write better

Just two rules: (1) Never use passive voice; and (2) Keep it simple. Don’t use two words where one will do. Don’t use a long sentence where two shorter ones will do. That’s it. Nothing more.

(1) First, understand whether your opponent’s opinion is changeable at all. Ask: “What specific data points, if true, would convince you to change your mind?” If nothing will, you might as well not waste your time arguing. [Aside: yes, the similarity to the scientific method is not incidental].

(2) Then, as Daniel Dennett says here, first restate your opponent’s view so clearly and succinctly that they wish they could have put it that way themselves.

(3) Then, call out the specific areas on which you agree with your opponent, and what you’ve learnt from their view.

Then, and only then, should you say even one word of criticism.

And yes, remember Miller’s Law. “To understand what another person is saying, you must assume that it is true and try to imagine what it could be true of.”

Before you say some statement is wrong or silly, first challenge yourself to think of a scenario where that statement actually makes sense. [The same principle applies for criticizing political decisions, competitors’ moves, etc.]

Finally, be happy to be proven wrong, like Darwin. Remember, you only learn when you lose arguments.

[Tweet “Be happy to be proven wrong. You only learn when you lose arguments.”]

c. How to give feedback better

There’s no playbook here.

Actually there is one – sandwich your feedback between two appreciative comments. It’s also known as The Shit Sandwich, and no, it doesn’t work. People see it coming a mile away. You start by saying “Your emails are always so well formatted”, and the opposite person immediately thinks, “God! How have I screwed up now?”

Instead, be authentic.

And come from the right place. Remember, you’re giving feedback so that the person succeeds going forward. And give constructive feedback frequently – don’t wait for review cycles, or the end of the week, etc.

In addition to all these, there’s one more important tenet to interpersonal communication. Always respond positively when someone says something to you. Negative / sarcastic reactions, or even no reaction at all, can be very damaging to relationships, as this article from Farnam Street recounts.

8. How to focus

This is an important one. Between emailing all day, getting pings on Whatsapp, and checking what’s new on Twitter, it’s a wonder we get any work done.

Even as I type this, my hand continually reaches out to check my phone. Maybe there’s a new message since I last checked 2 minutes ago?

As this article from the NYT argues, focus is a critical skill. And it’s incredibly hard in this age of digital distraction. But as Cal Newport shows in his book Deep Work, it can be learned.

How do we learn it? By practicing it:

First, use the Pareto principle. Take your to-do list, and remove the 80% of tasks that are unimportant.

Then, use Parkinson’s Law (“work expands / contracts to fill the time available to it”). Give yourself slightly less time than needed for each of the 20% important tasks. This will force you to focus – if you get distracted, you won’t be able to finish in the given time.

Of course, you’ll have to do the less important tasks at some point. For this, use a shallow work checklist that you tick things off when taking a break from the important tasks.

9. How to become a better manager

Read this FAQ from Henry Ward, CEO of eShares. Enough said.

10. How to get lucky

The last and final lesson I learned, and arguably the most important one. Building all those skills is great – it sets you up for success. But getting all the firewood together in one pile is not enough. Something has to light the fire. And luck is that matchstick.

Analogies apart (you can tell they’re my weak spot), you can acquire all the skills you want and work as hard as you can. But to win really big, you also need Lady Luck to favor you. And luck can be as capricious as they come.

But, like everything else above, you can engineer luck as well. You can expose yourself to positive luck, while limiting the downside from negative luck.

In the words of Nassim Taleb, you can be antifragile.

How do you do that?

a. Employ a barbell strategy – maintain a portfolio of low-risk / low-reward and high-risk / high-reward strategies.

Keep your day job, and try and build a side-business on the weekends. Quit your job only after the startup starts to scale. Even Craigslist was built in Craig’s spare time.

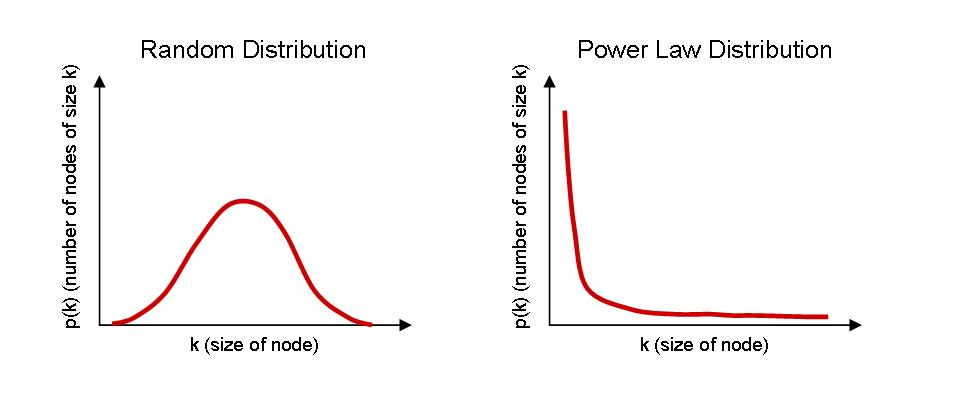

[Extra marks if you build your side business in a Power Law market. In such markets, if you do win, you’ll win huge.]

b. Build a strong network of ‘weak’ links – the best opportunities are at the edges of the status quo in every field. If you know people at the cutting edge in every industry, you’ll be better placed to spot and capitalize on big opportunities. Spend time with A+ people from other industries. [Note: This is also evidently the no. 1 predictor of career success].

c. Develop an “abundance mindset”. Look around and notice things. Be open to serendipity.

Nat Eliason has written a great primer on getting exposure to positive luck. You can also read this excellent book.

That’s it. Those were the lessons I learned from the 6,000+ articles I read in the last 52 weeks.

Over the last few years, I’ve been quite interested in the startup investing process.

At the trivial level, understanding the investing process could help struggling entrepreneurs (like me) raise funding faster. And, assuming that this investing philosophy does pick winners, this could also teach us what kinds of businesses tend to make it big. And we could then apply those patterns to our own businesses.

Marc Andreessen wrote a landmark article in 2007, on the only thing that matters. If you haven’t read it, go do so now. I’ll wait.

I re-read this article every few months. One line stood out to me the first time itself (and every time since).

He channels Andy Rachleff (Co-founder of Benchmark Fund, one of the most successful VCs) in his article, saying:

When a great team meets a lousy market, market wins. When a lousy team meets a great market, market wins. When a great team meets a great market, something special happens.

Thus, of the three key dimensions of a startup opportunity – market, product and team – market is far and away the most important aspect.

What’s the takeaway for an entrepreneur? Take aim at a humongous market, and put your head down and execute.

But is that true? Is targeting a large market the only important factor? Are the team, technology, etc. not as important?[1]

[fancy_box id=6][content_upgrade id=500]BONUS: Do you want this article as an easy-to-read PDF?[/content_upgrade][/fancy_box]

Is large market the most important factor?

It certainly is, according to the conventional wisdom. According to Andy Rachleff, again:

The best investments have high technical risk and low market risk. Market risk causes companies to fail. In other words, you want companies that are highly likely to succeed if they can really deliver what they say they will.

Don’t take market risk – i.e., aim for markets that are already large. Instead, take tech risk – where the product itself is hard to create.

This sounds great, and is a commonly accepted truism. And it also seems to be common sense.

But, again, is it true?

One way to settle this is to look at the performance of venture capital over time. As they say, nothing talks like money. But a quick look at VC returns can be quite sobering.

The Kauffman Foundation reports that VC hasn’t outperformed public markets since the late 1990s. In fact, since 1997, VCs have returned less cash to investors than they invested!

Could it be that this VC approach of taking high tech risk but low market risk isn’t working?

Tech matters (more)

I’ve just finished reading Crossing the Chasm, Geoffrey Moore’s landmark book. He presents technology adoption as a bell curve, with a few “gaps” between segments.

It’s easy to get the innovators and the early adopters. They want to be the first to try new technologies, so they’re primed to be convinced. You start hitting the main market only with the next group, the early majority.

Moore’s key insight is that it’s not natural to move from the innovators and the early adopters to the early majority. That’s why there’s such a huge chasm between these segments in the image above. A graveyard of companies that show great early traction, but suddenly hit a wall and collapse into the chasm.

His model suggests two pointers for technology companies:

Building a version of the tech, and serving innovators and early adopters, comes first.

The real challenge is crossing the chasm. You need to find a specific application to solve the early majority’s existing problems. This market isn’t visible or obvious at first – you need to create / discover it.

Thus, tech companies don’t take tech risk. They take market risk. If they find a big market, they succeed big. If they don’t, they fail.

Don’t take tech risk. Take market risk. If you find a big market, you succeed big. Else, you fail.

Jerry Neumann has written an excellent history of venture capital in the 80s. He makes a few similar observations (I paraphrase):

Whenever VC returns peaked, the driver was high market risk. Would there be a big market for computers (60s, Intel)? Would there be a big market for PCs (70s, Apple, Microsoft)? Would biotech become big (Genentech)? Would the Internet reach the masses, or would it remain a plaything of the elite (90s)?

These markets may seem inevitable today, but that’s just hindsight bias. Ask Ken Olsen. Or Thomas Watson. Or anyone in this article.

In most cases, investors didn’t take tech risk. Often, they found already-working products. Apple’s technology was already working when it raised funding.

Whenever VCs tried to reduce market risk to stabilize returns, they failed. For example, in the 80s, they entered more traditional, massive industries like retail. Result: returns were consistent and stable. But bad.

Thus, VCs didn’t often take tech risk. They preferred technologies that were already proven, and showed promise. And whenever they tried to reduce market risk by entering existing large markets, they failed.

At the end, Jerry summarizes:

The only thing VCs can control that will improve their outcomes is having enough guts to bet on markets that don’t yet exist. Everything else is noise.

There is no reason anyone would want a computer in their home – Ken Olsen, Founder, DEC

Peter Thiel’s Founders Fund adds its own voice to the argument. It highlights how, from the 60s to the 90s, VC was a predictor of the future. Today, though,

VC has ceased to be the funder of the future, and instead has become a funder of features, widgets, irrelevances. In large part, it also ceased making money, as the bottom half of venture produced flat to negative return for the past decade.

When you focus on incremental innovation, for a market that’s here and now, returns fall.

And last, Paul Graham makes a similar point, even more indirectly:

When something is described as a toy, that means it has everything an idea needs except being important. It’s cool; users love it; it just doesn’t matter. But if you’re living in the future and you build something cool that users love, it may matter more than outsiders think. Microcomputers seemed like toys when Apple and Microsoft started working on them… The Facebook was just a way for undergrads to stalk one another.

Build a product users love. Even if the market’s small today, it could become massive in the future.

I alluded to a similar point in a previous article, where I said that you must target a deep need for a narrow population, rather than a shallow need for a broad one.

[fancy_box id=5][content_upgrade id=430]BONUS: Get my checklist to identify bad startup ideas that sound good[/content_upgrade][/fancy_box]

What about the team, then?

As a VC friend of mine was quick to remind me when we discussed this, the quality of the team is incredibly important!

But this quality is not theoretical or bookish. It’s not about which Ivy League school you graduated from. Or even whether you have a string of successes under your belt (at least in consumer).

Instead, it’s about three things:

How driven you are. Will you overturn that 99th stone to find the gold mine? Or will the first 2-3 pivots fatigue you? Your initial ideas for tackling a problem will rarely be right. You’ll need to persist: find a new beachhead, and wade in again.

Are you willing to learn? Again, you won’t be right the first time. They say industry knowledge is a great unfair advantage. True, but it’s also a double-edged sword.

Can you execute?

So what’s the conclusion?

Which of these three is the most important?

The ex-consultant in me would answer, “all three”. And he’d throw in an “it depends” for good measure.

But it appears the conventional VC wisdom, of taking tech risk but not market risk, is wrong. As the Founders’ Fund article above says, the current trend of funding incremental innovations and more efficient solutions for existing markets is what has pushed VC returns downwards.

And what does this mean for entrepreneurs? Instead of trying to build something for large markets that VCs seem to be interested in, “swing for the fences”. But not in the conventional sense of aiming for large markets. Instead, try and piggy back on emerging trends that could become waves.

Sure, you’ll probably strike out. But should the market materialize, you will laugh all the way to buying the bank.

I’d love to hear your opinions. If you’re an entrepreneur or startup investor – what’s your stand on market risk vs. tech risk? Do email me at mail@jitha.me, tweet at @jithamithra, or comment here. I’d love to publish a follow-up sharing your opinions.

Thanks to Aditi Gupta and Abhishek Agarwal for commenting on drafts of this post.

[1] This article is about VC backable startup, and not a small business in general. Many great cashflow businesses (e.g., auto dealerships, general manufacturing) are often not high-growth businesses that can return 20x on invested capital, and are therefore not VC backable. See this article for a great description of such businesses.

Regular readers of this blog and my newsletter (subscribe here if you haven’t!) know that I’m an avid reader. 2015, for me, was a year of quantity. I read 60+ books, and at least ten times as many articles.

Some of these were bad, some good, and some changed my perspective on work and life.

I could list the top 5 books I read in the year. But instead, let me present the top 5 ideas that transformed my thinking, and the books I found them in.

1. Keystone Habit – One Habit to Rule Them All (The Power of Habit)

I’ve written before about Thinking, Fast and Slow, and the difference between System 1 and System 2 thinking. The former is rapid, automatic, instinctive and judgmental. The latter is slower, more considered and analytical, and more effortful.

In most situations, we tend to use the quick-and-dirty System 1. The more methodical System 2 is quite lazy.

This proclivity to use System 1 underlines the importance of habits. Such sequential, repetitive tasks are so ingrained that we do them without thinking. The essence of System 1.

For instance, do you think when you’re brushing your teeth in the morning? More likely you’re so woozy you can’t walk straight. Still, your teeth are sparkling clean by the end of it.

That’s the power of habits – you can do certain tasks without thinking.

To understand more about habits, I read two books this year – Hooked and The Power of Habit. They talk a lot about the structure of habits, how to build good habits, how to break bad habits, etc.

But the most powerful concept to me was that of the keystone habit. Keystone habits are small, narrow habits in one area of your life that impact several other areas in a significant manner.

As Charles Duhigg says in The Power of Habit:

Some habits have the power to start a chain reaction, changing other habits as they move through an organization. Some habits, in other words, matter more than others in remaking businesses and lives. These are “keystone habits,” and they can influence how people work, eat, play, live, spend, and communicate. Keystone habits start a process that, over time, transforms everything.

A few examples of this are:

Exercise. When you start exercising, even if only once a week, it triggers changes in various other areas. You start eating better. You become more productive and confident at work. You show more patience towards your family and colleagues. All because of a few push-ups once a week. That’s a keystone habit.

Making your bed every morning. It’s a tiny, almost irrelevant change. But studies show that this correlates with better productivity, greater well-being, and more willpower.

Willpower. This is the most important keystone habit. Studies show that willpower in children is the most accurate indicator of academic performance throughout their student lives. Even more accurate than IQ.

At an organizational level as well, keystone habits can have transformative impact. The book cites an example of how a worker safety program at Alcoa ended up not only improving safety, but also turning Alcoa into a profit machine.

How do these small, unrelated habits have such widespread impact? In Duhigg’s own words:

Small wins fuel transformative changes by leveraging tiny advantages into patterns that convince people that bigger achievements are within reach.

So what are your keystone habits at life and work?

[fancy_box id=5][content_upgrade id=463]BONUS: Get my 2016 Reading List with 40+ book recommendations![/content_upgrade][/fancy_box]

2. Rewards and their Unintended Consequences (Drive)

Incentives are strange, powerful beasts. Whether it’s pocket money we give children for doing household tasks or bonuses our bosses give us for exceeding sales targets, incentives play a key role in driving us to perform.

I think I’ve been in the top five percent of my age cohort almost all my adult life in understanding the power of incentives, and yet I’ve always underestimated that power. Never a year passes but I get some surprise that pushes a little further my appreciation of incentive superpower.

Given the immense power of incentives, it becomes all the more important to design them right. If they’re even slightly misaligned, they can “damage civilization” (Munger’s words, a tad hyperbolic).

I read Drive earlier this year – an insightful book on the powers of rewards. The book also talks about the negative influences of incentives, if not designed well.

Incentives can drown out intrinsic motivation, even when you’re doing a task you enjoy. If you receive an incentive for doing something, you also receive a subliminal message that the task is not worth doing without the incentive. End result: incentives transform an interesting task into a drudge, and play into work.

[Tweet “Incentives transform an interesting task into a drudge, and play into work.”]

Incentives can only give a short-term boost. Like caffeine, they’re useful when a deadline looms. But beware the energy crash that will inevitably follow.

Rewards can become addictive. As Daniel Pink, the author, says – Yes, rewards motivate people. To get more rewards.

Incentives do have their uses, but only for process-oriented tasks. In fact, incentives for creative tasks can impede progress. They narrow your focus at the exact moment when you need broad thinking.

The book captures many more interesting and significant implications of an innocuous, innocent incentive.

3. Your MVP can be more “minimum” than you think (Lean Startup)

Most people working in the startup ecosystem are familiar with the Minimum Viable Product. The MVP is the most basic version of your product that still delivers your core offering.

It’s an important concept to keep in mind as you build a product. You don’t want to spend too much time building the first version, before realizing customers don’t want it.

I thought I’d understood the concept well. I congratulated myself as I built my first product in three months, found that people didn’t need it, and junked it. And again when I built my next product in four months, tested it with customers for three, and then pivoted it to its current form.

Then I read Lean Startup.

I realized then that I’d taken far too long to build my MVP. What’s more – so had everyone else I know. Why do we all take so damn long to build an MVP?

The reason is that we’ve got the concept wrong. You don’t need to ‘build’ an MVP. You just need to put it together.

What does that mean?

Let’s say you want to create a website offering fashion tips. You can launch in one day or less.

Buy a domain. 3 hours (the actual purchase will take 2 min. But I know you’ll agonize over names for the remaining 2 hours 58. And no, the name won’t matter.)

Build a landing page with Unbounce where people can ask questions or upload photos. 1 hour.

Run a small Facebook campaign publicizing the site. Or tell 10 friends, and tell them to tell 10 more each. That’s your test audience. 2 hours.

Thus, you can be up and running tomorrow! Even if you’re slow because this is your first time.

[Tweet “Your Minimum Viable Product can be more “minimum” than you think.”]

Many popular products of today hacked together such makeshift MVPs when they started. Check out the article in Further Reading for examples.

4. Pareto Principle & the Minimum Effective Dose (Four Hour Work Week)

Four Hour Work Week, by Tim Ferriss, is THE book to read on personal and business productivity. Unlike most productivity books and blogs, he eschews all the standard life-hacking methods (of the “shake your hips while you brush your teeth, to get some exercise” variety).

All he has to say about traditional time management is, “Forget all about it.”

[Tweet “All you need to know about traditional time management is, “Forget all about it.””]

Instead, he focuses on using the Pareto Principle, or the 80/20 rule. He uses this to introduce the concept of the Minimum Effective Dose – the smallest amount of effort for the most impact.

Whether your customers, your vendors, books you read, anything – choose the few that give you the most value, and forget about the rest.

He should know. He puts the Pareto principle on steroids. Sample this:

In his nutrition products business, he “fired” the least profitable 97% (!) of his customers, to instead focus on the 3% most promising ones and double his income.

He eliminated 70% of his advertising costs and almost doubled his direct sales income.

He discontinued over 99% of his online affiliates.

Eliminating the least value tasks and business relationships helped him free up his time to do more productive tasks. And achieve the Holy Grail of less work but more profit. That’s how you do productivity!

Side note: In his follow up book, The Four Hour Body, Ferriss uses the concept of the Minimum Effective Dose to illustrate how to become more healthy. Check that out too.

One skill I tried to build last year was negotiation and persuasion. I read three great books on the subject. I’m still to have the investor conversations where I’ll use this skill, so I don’t know how much they’ve helped!

But one concept that has stuck is that of the BATNA – the Best Alternative To a Negotiated Agreement. In simple terms, the BATNA is your fall-back option in case talks fall through.

Your BATNA is tantamount to your leverage in the negotiation. It works in two ways.

1. The better your BATNA, the more leverage you have.

Let’s say you’re negotiating the sale of your house with a prospective buyer. Your alternative to this is to (a) rent it out; (b) sell it to a land developer to make a parking lot, and (c) live there yourself. If option (b), say, is the most attractive of these, then that’s your BATNA. The value the land developer offers you should form the baseline for the negotiation.

As long as the buyer’s offer is higher than this, you can reduce your price (after making a big deal of it, of course).

Far more important though, is that if the buyer pushes you below this BATNA, you can and should refuse. This is difficult. We tend to over-invest emotionally in a long negotiation. But with this hard stop in mind, you can overrule your emotions and walk away.

2. The worse you make your opponent’s BATNA, the more leverage you have.

Improving your BATNA gives you leverage. Straightforward. But there’s a more interesting insight here. You can improve your leverage by worsening your opponent’s BATNA.

Let’s say you’re the prospective buyer in the above transaction. You know that your seller is holding out because of the safety net of the land developer.

So, you remove that safety net. For example, you could sell one of your own other properties to the land developer, so he’s no longer making an offer to your seller.

By removing the most promising alternative your seller has, you’re weakening his leverage. And strengthening your own considerably.

[Tweet “Show your opponent he has a lot to lose from breaking talks, and he’ll be surprisingly pliable.”]

6. [BONUS] Focus on strengths, not lack of weaknesses (The Hard Thing about Hard Things)

By default, we are all risk averse. In fact, Loss Aversion is one of the strongest, most deep-rooted cognitive biases there is, squirming deep inside our brain’s reptilian core.

This loss aversion manifests itself in several ways. Holding on to bad-performing stocks in the hope of a turnaround. Not making bets because of high risk, even if the reward is much higher.

In the corporate environment, this results in a preference for well-rounded candidates. We tend to choose such people over others who are spiky in some areas, but middling in others. We choose average programmers with great communication skills over 10x programmers who are introverts. We reject uber-salesmen just because they don’t know much about tech.

As Ben Horowitz says in this book, that’s the exact wrong approach. That’s not how great organizations work. Instead, such organizations look for excellent candidates, who are in the top 1 percentile of their roles. Never mind that they’re not good at other things.

“Identify the strengths you want, and the weaknesses you’re willing to tolerate.”

Your Product team should have the best programmers. Even if their communication skills could be better. For sales, hire the best salesmen out there, even if they’ve not worked in your industry before.

We also tend to paper over the weaknesses and focus on repairing them. Again, not the most optimal approach. Instead, focus on honing your employees’ strengths. Plug the weaknesses (If they’re important. They often aren’t.) by hiring superstars in those areas.

[Tweet “Identify the strengths you want, and the weaknesses you’re willing to tolerate.”]

[fancy_box id=5][content_upgrade id=463]BONUS: Get my 2016 Reading List with 40+ book recommendations![/content_upgrade][/fancy_box]

So, those were the books and ideas that captivated my thinking in the last year. Here’s to many more brilliant ideas and books in the new year. Of course, you’ll be the first to know of any great books I find (sign up here to receive regular updates!).

I read this post by Ellen Chisa recently, on the most important things she learnt at Harvard Business School. While I did not go to Harvard, I still had the good fortune of going to IIM Ahmedabad. So Ellen’s post motivated me to compile my own list of learnings from business school. But that was only part of the inspiration. There’s a standing joke, not entirely funny, among IIM graduates that many of the top schools in India are just glorified placement agencies. I thought this was an opportunity to check if that’s true. So, did I learn anything at all from my two years at business school?

As I started reflecting on my learnings, I thought – why not crowdsource some opinions and round out the article? Plus, there’s a conflict of interest in including only my learnings – I have a blog post to complete, and would be ready to manufacture some lessons if required! But my friends and classmates would have no such motivations.

Accordingly, I put this vaguely worded question to a bunch of my classmates and friends. And interestingly enough, everyone who answered assumed I meant only non-academic learnings – and replied with timeless meta-lessons like ‘importance of networking’, ‘big picture thinking’, ‘knowing you can push your limits’. This was as strong an indicator as any that this belief – that there’s not much learning to be had from business school academics – is very pervasive. Of course, on some prodding, they did highlight some of their more influential takeaways from the course subjects.

Accordingly, I’ve put together a compendium of the top ten things we’ve learnt from business school – both academic and non-academic.

Let’s start with the academic learnings first:

1. Time value of money

As a young engineer without work experience, it was quite a revelation for me that the value of money grows with time – a rupee today is not the same as a rupee one year from now. And if you leave your cash just lying around (or in a zero interest account), it’s actually losing value. At minimum, you should try to earn a risk-free interest rate on it. I knew banks paid interest on your deposits, of course, but I hadn’t realized that should be the bare minimum.

A corollary of this is that the best use of money (other than spending it) is to make more money – make your money work for you, as financial gurus say. While this hasn’t been life-changing, it has significantly influenced how I treat money – I’m always looking for places to invest it, rather than leaving it idle in my account. And I know many classmates who keep very little money in their savings account – almost everything is invested! I can’t go to that extreme – there’s enough stress in my life as it is.

2. Value of time

But while I’m always looking for investment avenues, I’m also looking for an easy bet. I’d rather invest in a low-cost fund that just invests in the stock market index, than plough through lists of the 100 best mutual funds or research 50 undervalued penny stocks, even though the latter strategy may outperform the index by half a percentage point. Why? Because my time has value too.

This concept, of opportunity cost of time, was also something that business school introduced me to. When spending time on a specific pursuit, it’s also important to consider what else you could be doing with your time, and the value of that. When starting up, the employee salary you forego is the opportunity cost. When you invest money and developer time on some product features, it is at the cost of other potentially lucrative features. When you choose to do something, you’re also choosing NOT to do something else.

[Tweet “When you choose to do something, you’re also choosing NOT to do something else.”]

On a related note – I don’t watch TV shows. I don’t want to lock myself into watching 5 seasons of a show – there are many more useful things I could do with 50 hours of my time. (OK, it’s not completely related. But I did want to make the point that this week’s Game of Thrones spoiler didn’t affect me one bit).

A concept that is more related, though, is sunk cost. This was a very useful lesson as well – that how much you’ve already invested in a particular project shouldn’t matter in a decision of whether to continue. What matters is only future investment, payoff, and the opportunity cost of continuing. I understood this fairly well as a concept, but I properly internalized it only when my first product idea was tanking – and I faced the choice of continuing to invest or trying something else. I’m happy to say I dropped it like a hot potato. Or like I stopped watching Prison Break after one season (I promise this is the last TV show example).

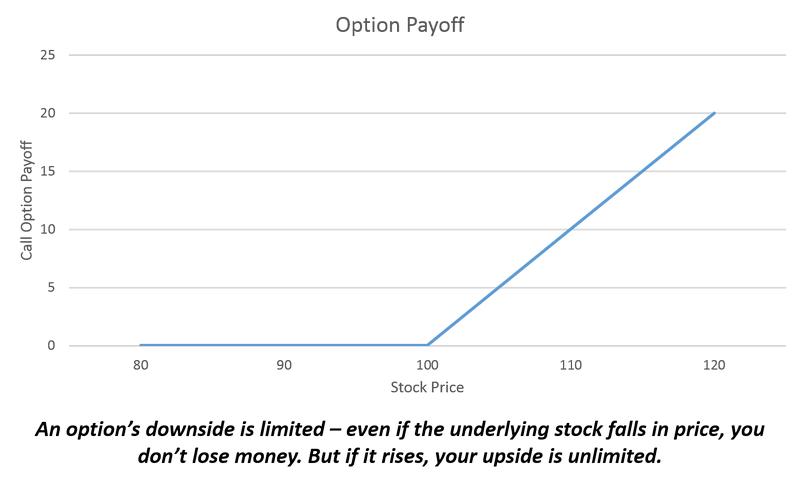

3. Value of optionality

One of the most popular courses in the 2nd year was FORM, or ‘Futures, Options and Risk Management’. Everyone made a beeline for this course, primarily because it had high signaling value if you wanted an investment banking / trading job out of campus. The main topic in FORM was the Black-Scholes formula for pricing an option. But it sure wasn’t my main takeaway – Black-Scholes was BS (and I don’t mean just the acronym). Rather, I took away the sheer value of having an option – of limiting your downside but having potentially unlimited upside.

This is very similar to the concept of making a skewed bet, which I posted about here. Having an option is a great mechanism to reduce risk, which, counterintuitively, is exactly what you need to do when taking risks.

[Tweet “If you’re taking risks, look for ways to reduce risk.”]

[A sidenote: I was so taken by the concept of options in my 2nd year that I created a blog called optionalityrocks.blogspot.in. It still exists, with a grand total of two posts, the last of which was in 2009. Still, I have the option of posting there.]

4. The usefulness of frameworks or mental models

This learning wasn’t from one particular subject. But across courses, one thing I noticed was that using frameworks – like Porter’s Five Forces, 4 Ps of Marketing, etc. – made it very easy to understand intricate concepts and analyze complex business situations. Using a well-established framework makes solving a business problem far more efficient – it takes far less time than approaching it from first principles, and also ensures that you don’t miss any important factors.

Much to my dismay, I didn’t use the Five Forces framework much in my working career, even though I joined the consulting firm that Porter started. Still, there were many other, less outdated frameworks that I used there, and today, one of the first steps I take when approaching a problem is to choose a mental framework to apply to it – it helps me arrive at a more well-considered answer, far more quickly.

This concept is very similar to Charlie Munger’s mental models, which Warren Buffett, his partner in crime at Berkshire Hathaway, highlights as a key contributor to his investing genius.

5. Excel

This is not a concept, as much as learning a primary trick of the trade. Ever since Harvard pioneered the case-based learning method, many schools adopted it to cultivate more practical, less bookish managers. But a common mistake they made was to focus far too much on the big picture, while eschewing more on-the-ground tools. Sadly though, your first post-MBA job usually isn’t as a visionary CEO – you need to work in the trenches. And Excel modeling is an important tool to obtain actionable insights for your company. Thankfully, Excel training was a key part of the IIMA syllabus from the very first term – something that helped students hit the ground running in their first jobs, and differentiate themselves from recruits from other schools.

These were my academic learnings from IIMA. Some of my friends highlighted HR, Communications, etc. as subjects that helped them understand how to work with teams better. However, I’m unable to separate the influence of these subjects – I think I learnt far more about people management in my first job. I may be biased, but I’m going to leave them out.

Right, let’s move on to the more interesting stuff, shall we? What else did I learn, outside the classroom?

6. Time management and prioritization

One thing that hits you very soon after you start at IIMA is the ridiculously false sense of urgency to everything. You have a surprise test on your very first day of class (not very surprising – evidently happens every year). You have a submission or two in your first week, and a group submission (with people you hardly know) within the first two. And this pace doesn’t let up for the whole first year.

Apart from making you shake your head in disbelief, this also helps you learn about your limits, and how much more you’re capable of than you assumed. Functioning efficiently on 3-4 hours of sleep for days on end, juggling multiple submissions on any given day or running from one end of the campus to another to get your submission in before the deadline – all of these teach you how to manage your time and get things done. And the next time you face a real life crunch, you have the confidence that you can deliver, even on two hours of sleep.

7. Importance of team work

Team submissions are an important part of the syllabus, accounting for a major portion of one’s grade. If the case-based instruction approach and open book problem-oriented exams aren’t enough motivation to snap out of bookish learning, then the assignments force you to work in teams – even if you’re narrowly interested in scoring marks, you need to work with other people. You need to extend yourself to paper over their weaknesses, as surely as they do to mask yours.

Clichéd as this may sound, working with others under constant pressure teaches you a lot about yourself and your weaknesses in team settings, giving you a chance to improve and be more ready for the real world.

8. Always strive to be around people you can learn something from

This was a very strong personal learning for me. After doing quite well academically in my own small pond, I had delusions going into IIM about how well I would do there. The first month was quite a brutal wake-up call – everyone around me was much smarter. But after the initial shock of this new normal had subsided, I actually started learning a lot from them. Those two years became a time of huge personal growth for me, and I resolved to (a) always be learning; and (b) always be around people I can learn from.

It’s serving me fine so far – there’s far more opportunity in this big sea than in my small pond.

9. Perspectives can shift very easily

One thing that surprised me during my stint at IIM, especially the first year, was how easily people’s frames of reference changed. Just like the famous Stanford prison experiment, the artificial pressure changed people into strange beasts. Perfectly genial guys stopped sharing their course notes and otherwise calm folks couldn’t sleep nights, all agonizing over one measly relative grade that may or may not influence your future career (it hasn’t yet, in my case). It was incredibly hard to retain perspective. But this was, after all, just a 2 year academic course that YOU paid for, and you’d already crossed the biggest barrier to getting a great job (i.e., getting into IIM). So chill out, and focus on learning and making friends for life.

Luckily for me, I had very grounded friends in my dorm, who couldn’t be bothered to get too tense about a surprise test or a term-end exam. We all did well academically, but without losing our cool. For that, I’m thankful.

10. You can game your way through anything. The question is – do you want to?

Rigorous though the B-School curriculum feels, there are ways to fraud your way through. The 80-20 rule applies, and you can easily get a half-decent grade without studying too much. I’ve not studied at an IIT, but I’m told that’s not very different either. Honestly, the grades don’t matter – so it’s fine either way. But what matters is whether you want to learn, or you’d prefer to rest on your laurels. You’ll get a good job anyway, sure, but your professional approach gets molded in these formative years.

Of course, I’m seemingly imparting sage advice now, but even I joined a management consulting firm from campus – something Paul Graham of Y-Combinator advises you to do only if your true calling is gaming the system. I don’t fully agree, but I hope I’m making amends now by voluntarily struggling.

Those were my learnings from B-School – concepts I apply in my daily life of which I can genuinely say – Yes, I learned this at IIMA. Would love to hear your thoughts – what did you learn from your B-School stint? Comment here, drop me a line at gt.jithamithra@gmail.com, tweet at jithamithra, or heck, write your own blog post and send me a link. Look forward to hearing from you!

Hello! I’m finally back to blogging, after a short hiatus to focus on my app’s launch. It’s been a topsy-turvy few weeks with several delays, but we’re now only a week away from launch. Hopefully.

Delays beyond your control can be quite deflating when you’re waiting for the culmination of months of effort. But it’s at times like these that it’s most important to keep your shoulders to the wheel – even when things are not fully in your control, you need to do everything you can.

In this sense, the last few weeks have been a microcosm of the entire starting up experience – unless you’re Elon Musk, luck and other external factors will play a significant role (often more than your otherwise significant efforts) in success or failure. What you can do, is stay on the field. And that requires motivation.

Motivation is a strange beast. I used to think that decent pay and bonuses are good motivators, but here I am, grinding away with no income. And I’m enjoying myself. Clearly, there are some intrinsic factors at play that keep struggling entrepreneurs in the game (hopefully not foolhardiness though).

I’ve wondered about this quite a lot over the last 2 years. But a lot of my questions were answered when I read Drive a few weeks ago. This book, written by Daniel Pink, explores what really motivates us, based on findings from scientific research. [Hint: it’s not money and bonuses]. I’d recommend this book to everyone – understanding what motivates people has pretty direct implications for how we manage our employees, our bosses, our customers, our families, and everyone else we interact with on a regular basis.

But this isn’t a book review or summary. Ever empathetic to the busy reader, Pink himself has included summaries (both Twitter and cocktail party variants) at the end of his book. Instead, I would like to dwell a little on one aspect – his discussion on extrinsic motivation. I found it fascinating to understand some of the pitfalls of extrinsic ‘carrot’ rewards like money and bonuses.

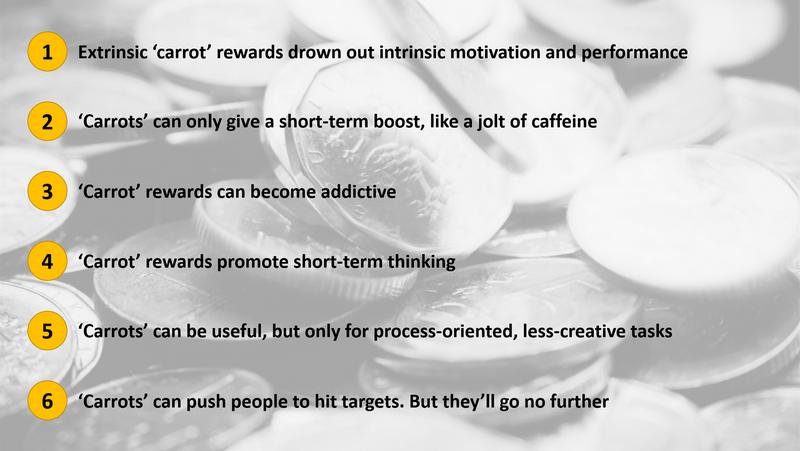

1. Money drowns out intrinsic motivation and performance.

Research shows that even if you innately like a task, being paid for it actually reduces how much you like it. I was surprised by this result, but some others intuitively get it. For example, one person I know loves baking in her free time, but doesn’t want to do it full-time – she feels that the pressure of earning money will reduce the pleasure she gets from baking.

Rewards perform a weird sort of behavioral alchemy – they can transform an interesting task into a drudge, a fun assignment into a bore, and play into work. And by reducing intrinsic motivation, they can send your performance and creativity toppling like dominoes. What’s more, you’ll now only do these tasks if you’re paid for them. [Note to parents – don’t pay your kids for household chores]

[Tweet “Money can transform an interesting task into a drudge, and play into work”]

2. Extrinsic rewards give a short-term boost. Like a jolt of caffeine, they’re particularly useful when a deadline is looming. But like the energy crash that inevitably follows a post-coffee frenzy, long-term motivation and performance will also fall.

3. ‘Carrots’ can become addictive.

Offering an extrinsic monetary reward for a task signals that it is undesirable (if it were desirable, would you need a carrot?). And this, to resort to cliché, is a slippery slope. Offer too small a reward, and they won’t comply. But offer a reward that’s enticing enough the first time, and you’re doomed to offer it forever.

[Tweet “Yes, rewards motivate people. To get more rewards.”]

But the bad news doesn’t end there. Once the initial money buzz wears off, this will feel less like a bonus and more like the status quo. You’ll then have to offer ever-larger rewards to get the same task done, just like the nicotine addict falls into the vicious cycle of more and more cigarettes to get his ‘hit’.

4. Rewards promote short-term thinking

Once there’s a carrot in front of you, that’s all you’ll see, at the expense of more long-term objectives. Just like the auto mechanics who conduct unnecessary repairs to meet their sales quotas. Or, more terrifyingly, Delhi’s monster Blueline buses which went on a killing spree, all because of an innocuous incentive to ply their routes quickly.

5. However, extrinsic rewards aren’t completely useless. If the task at hand is process-oriented, like filing documents into folders, then an incentive can speed you up and reduce your Facebook / power nap breaks. But if a task is creative, then monetary rewards have the effect of narrowing your thinking – when what you require is the exact opposite.

6. When you attach a bonus to a target, you may increase the probability that it will be hit (at least if the task is process-oriented). But you almost guarantee that the target will not be surpassed. Your teams will work hard to meet the target. But no further.

Thus, over a basic threshold of the amount needed for basic comforts and happiness, monetary incentives can work negatively. This has deep implications for how we manage our teams, employees, families, etc.

We could now talk about what does motivate people. But why don’t you read the book for that? Let’s do something more interesting instead – let’s predict what these findings mean for some of the trends in our economy.

b. Many heavily funded startups are spending equally heavily to acquire employees and customers. But these efforts may have a short shelf life.

If you’re throwing money at employees, you should expect that you won’t retain them over time, and that performance will suffer in the interim. Unlike large companies, work at startups is not algorithmic and process-oriented – you need someone who reigns in (and reins in) chaos.

In their bid to conquer the mobile space, many companies are incentivizing app downloads by the millions (yes, users actually get paid for downloading apps). Even if these investments boost vanity metrics today, results will tail off very quickly, as users begin to install apps just for the rewards, and then never use them again.

c. If you do have to use incentives, design a mix of long- and short-term targets, and make them harder to game.

App marketers could incentivize use of the app over time, and not just installs. Give a bonus on the first major activity, rather than on ‘Install and use for 30 seconds’.

In a corporate sales scenario, bonuses could be driven by both new sales and customer churn, to promote longer-term customer management vs. one-time discounts.

d. But even when promoting use, a monetary incentive is bad news. Just like Drive showed, if you create incentives around specific targets, people will work hard just to meet them, and no more.

A case in point is the Indian government’s drive for rural toilet construction (a strong interest area of mine – see this). Over the last 15 years, the government has given ever-increasing incentives for toilet construction – starting with Rs. 200-400 in the early 2000s, to Rs. 12,000 today. But they’ve seen large numbers of toilets being used as anything but – often as store-rooms or an additional room. People have just constructed ‘toilets’ to pocket the incentive.

Yes, this is a toilet!

Many stakeholders are now trying to move the incentive towards usage – e.g., a part of the reward comes to you only if you’re still using the toilet 3 months after construction. While this idea sounded great the first time I heard it, I now fear it may also be doomed to fail. This effectively destroys intrinsic motivation to use a toilet (which there otherwise would be – it is indeed far more convenient than open defecation). People will feel they’re being paid to defecate at home because that’s the less comfortable thing to do. When the incentives stop, use will fall too. Bringing us back to square one.

Extrinsic rewards are undoubtedly simpler to design – what’s easier than throwing money at a problem, in these profligate times? But Drive serves a timely reminder that as in most other areas, only the hard work of creating intrinsic motivation will bear fruit.

Hope you found this post interesting. Can you think of any other implications of extrinsic ‘carrot’ rewards? Do share in the comments. You can also email me at gt.jithamithra@gmail.com or tweet at @jithamithra. Until next time, then!

We constantly read about companies that have created barriers to entry – through technology, intellectual property, large-scale manufacturing, or sometimes even by throwing a ton of money at a problem. For startups, this barrier to entry is a constant refrain, especially in conversations with potential investors – “What’s your barrier to entry? What asset are you building that’s hard to replicate?”. And this is a hard question with no easy answers, especially for a young company that’s not building a high-tech, proprietary product – a bigger competitor with deeper pockets could appear at the ramparts anytime, and replicate exactly what you’re doing.

But what if just focus on a particular user segment could help you develop a competitive advantage? What if expending all efforts to serve a particular market niche or user segment could help you unearth a resilient barrier to entry?

I read a book called ‘Good Strategy Bad Strategy’ last year and was struck by how insightful it was. I’ve revisited my notes from the book at least twice now, each time capturing a new nuance. It’s a must read for students of strategy, advisors on strategy, and practitioners. Having been all three (in that order, oddly enough), this is right up my alley.

The book had many great ideas on sources of power for companies – what gives a company lasting supremacy in its market. One idea that stayed with me was of single-minded focus – how focus on a particular type of user can be a sustainable source of power or competitive advantage. How would this work? Let’s dig in – this feels like another 1800 word post.

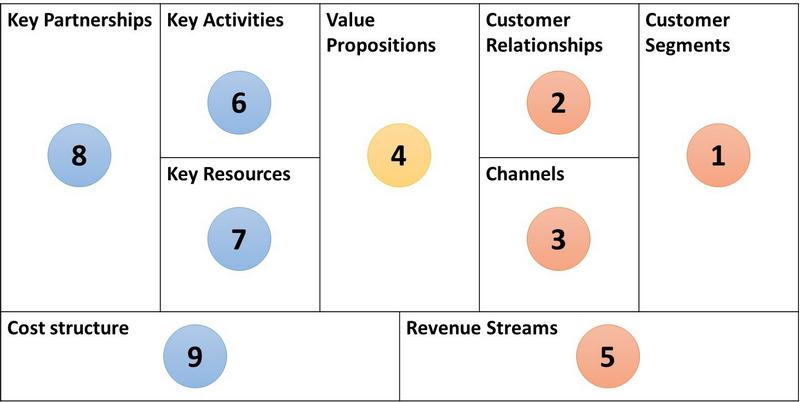

Any company’s business model has 9 different parts, as below:

Source: Strategyzer.com

The author, Richard Rumelt, points out that to focus on a specific user segment, you need to make coordinated changes across multiple or all parts of your business model. Thus, your final offering to the customer is a sum of many moving parts that have all been finely configured – a sum that, as the cliché goes, is more than its parts. Applying such focus takes incredible coordination of policies, which, along with their interlocking and overlapping effects, can then confer unassailable advantages and make you a hard act to follow.

I know this seems very philosophical (a little like bad strategic advice!), so let’s look at a few examples to illustrate this better:

1. IKEA

Rumelt uses the example of IKEA to illustrate this concept. IKEA is a furniture retailer that sells ready-to-assemble furniture. It targets do-it-yourself or DIY users, who love the feeling of putting something together. It has been hugely successful across multiple countries, but 70 years since its founding, no credible competitor has appeared or lasted. That’s sustainable competitive advantage!

IKEA has no secret sauce in terms of patented technologies for furniture, greater marketing strength, etc. The source of IKEA’s lasting advantage is, instead, the coordination between the different elements of its business model to serve its target segment. For a competitor to challenge IKEA, they don’t just have to sell ready-to-assemble furniture – they’ll have to change their whole business model.

They’ll have to design new types of furniture;

They’ll have to start carrying larger inventory;

They’ll have to create their own, branded stores; and

They’ll have to change their selling models.

Thus, copying IKEA is not a simple matter. IKEA’s policies are so different from the norm in the furniture industry that any competitor would have to replicate ALL of them to meaningfully compete for the same user segment. Adopting one or two of these policies and implementing them, even perfectly, would be useless – it would add huge expenses without providing any real competition.

2. Apple

Apple is another example. Over the years, Apple has targeted its products at premium customers who want a superior experience – well-designed products that just work. They’re not interested in the most technologically advanced products with the most bells and whistles – they want products that do their job simply and well. Oh, and there’s snob value too.

Apple has made several interdependent decisions to target this group:

Complete ownership of the product: Take the iPhone. Unlike its closest competitor, Android, Apple controls the entire product – the OS, the hardware, user interface, etc. This allows it to deliver a very coordinated and quality user experience.

Complete ownership of computer ecosystem: Moreover, Apple coordinates the experience across all its products. The Apple ecosystem can satisfy all your computing needs – desktop, laptop, tablet, phone and music player. All of these products follow the same design language, and work together seamlessly – they sync with each other very easily, without any need to fiddle with system settings.

Branded retail stores with a luxury experience

Marketing mainly to premium customers who don’t mind spending more – this not only raises product revenue, but also increases the long tail of revenue from app store downloads, music downloads via iTunes, etc.

The reason Apple’s position in the market is unassailable is that a competitor can’t just copy one or two things to start selling to the same group of customers. The competitor would have to copy everything, a formidable task even for very nimble companies. And copying sequentially won’t work – you can’t begin to deliver the Apple or IKEA value proposition without copying everything from the outset, in a coordinated manner. Which is why, even though Android and its partner OEMs have copied a lot of product design elements from Apple (in fact, the first Samsung Galaxy S was an iPhone in all but name), they haven’t been able to displace Apple from its position as the proprietor of all things cool.

Thus, the business models of IKEA and Apple are like a chain – multiple independent elements interlock to engineer a truly durable value proposition. As for a competitor, the flipside of a chain-linked model applies – your proposition is only as strong as your weakest link. Focusing on strengthening just one or two aspects of your model won’t increase your ability to compete even one bit – you need to strengthen everything, all at once.

Let’s try and apply this mental model of a chain to a few other sectors. Are there other companies as well, which have used focused, chain-linked business models to derive competitive advantage?

3. Wal-mart: In the 60s and 70s, Sears and Kmart dominated retail. But they mainly served large towns or cities that could ‘support’ a large retailer. Wal-mart changed the game by creating large-format stores away from cities, allowing enormous spaces at lower costs. It positioned itself as a ‘discounter’, something other players avoided like the plague. And it was able to make money while offering deep discounts, through several interlocking innovations:

Extremely wide product portfolio with deep discounts on some products, cross-subsidized by other high-margin products

Cutting-edge technology to track customer purchase behavior, and tailor portfolio accordingly

Agile supply chain, keeping its stores well-stocked with the right products very efficiently

Thus, several innovations, all focused on offering products at the lowest prices, gave Wal-mart lasting competitive advantage. By 2002, Wal-mart was the largest retailer in the world, and Kmart was bankrupt.

4. Dell: If you wanted to buy a desktop in the US in the 80s or 90s, your only options were to either buy a standard configuration through a retailer, or buy individual PC components to customize the machine yourself. Unless you built the PC yourself, you did not get much choice in the product or configuration you wanted. Dell saw an opportunity to change this by offering customized configurations, and thereby targeting the more technologically adept consumer.

Dell took a number of hard decisions to make this happen. It created an easy to use online / phone interface for users to configure computers of their choice. It delivered this promise through a mass customizing production process, and built a direct-to-customer distribution channel. None of these decisions were easy to replicate even singly, much less in lockstep. The result – a lucrative business model that stood unchallenged during the PC boom of the 90s.

OK, these are standard business school case studies. Let’s look at a few newer companies.

5. Innocent: The British healthy drinks / smoothies player has built a strong position in its home market. Innocent offers health-oriented users very fresh fruit-based drinks – their promise is, zero preservatives, only natural fruit. Offering this focused proposition means a number of business model decisions – sourcing the best fruits only, producing for short shelf life, faster cold chain logistics to get the product to retailer shelves very quickly, and so on. All separate decisions, coordinated to deliver user value. Competitors have found it very hard to replicate this – Pepsico, after years of trying to compete in this market, finally bought a smaller competitor to gain a toehold.

6. Zara: Zara has carved itself a preeminent position in the ‘fresh fashion’ space. Zara’s stores are always stocked with the latest trends – Zara gets clothes from design to outlets in 10-15 days flat. And it has done this by tailoring multiple parts of its operating model to accentuate this speed:

Much larger design team than other apparel brands – its 200 designers ensure a steady flow of new designs, taking advantage of the latest trends and feedback from customers.

While most apparel brands manufacture in China, Zara manufactures in Europe close to its main markets – this gives it a head-start of at least 1.5-2 months.

Short production runs, with limited quantities – Zara doesn’t run more than one production cycle for most of its products. If a particularly striking outfit runs out at its stores, that’s it. You won’t see it again. From a user’s point of view, this drives a purchase decision faster. If you plan to come back tomorrow to buy a dress, it may not be there.

Putting these aspects together, other brands find it very difficult to catch up with Zara – all of these are major business model revamps that are difficult to pull off, whether alone or in coordination with each other.

These and several other successful companies show that focus and coordination can create a massive barrier to entry and lasting competitive advantage, keeping challengers at bay for years to come. It’s a telling reminder to businesses – you don’t need cutting-edge technology or a massive fund-raise, just good old-fashioned customer service will do!

What do you think? Are there any other consequences – positive or negative – of focusing your business model on a specific user segment? Would love to hear from you – mail me at gt.jithamithra@gmail.com, tweet at @jithamithra, or comment here on this blog. And do subscribe here – I post roughly once a week, on startups, business models, consumer behavior, etc.

PS. I’ve just started a newsletter called The Startup Weekly with Abhishek Agarwal, a close friend, curating the most interesting articles, case studies, etc. for startups that we come across every week. Would be a good addition to your inbox (so much for conquering it). Sign up here – first issue goes out this Saturday!

Retailers try many tactics, some obvious and others devious, to take advantage of our buying habits and maximize how much we purchase. They also use purchase data and buyer demographics to identify their most valuable customers, and make them purchase more. Nothing surprising there. But what’s interesting is that across retailers, one customer archetype is consistently the most valuable – pregnant and new mothers.

I recently read The Power of Habit, which outlines the process by which we form habits and explains how we can modify them or create new, more constructive habits. It’s a fascinating and insightful read, and I’m going to try changing some of my habits using this framework (no more candy for me!). But this post is not about the habit process (read the book, lazy people!). The book had a very interesting chapter on retail habits, and how retailers take advantage of them.

Some of these retailers’ tactics are pretty obvious – think of how you have to walk all the way across the mall in search of a staircase. Studies have found that over 50% of your purchases are impulse buys – and this is if you made a list beforehand! So, making you walk across the mall, seeing more products than you would otherwise, will make you purchase more. Slightly more devious is how supermarkets keep fruits and vegetables right near the entrance. If we stock up on healthy stuff right at the start of a shopping trip, we feel great about ourselves and are much more likely to stock up on chocolates, biscuits, chips, ice creams, etc. when we encounter them later. There are many more such tactics employed by retailers to take advantage of our habits – you can see a few more here.

These habits – buying what we see, weakening after buying healthy products, etc. – are ingrained, as are our choices for where we buy specific products. Tactics to take advantage of these habits are now table stakes. But where retailers can make the most impact is when habits change. And even ingrained habits change – typically during some major life change or emotional upheaval.

For example, when people get married, they’re more likely to start buying a new brand of coffee. When they get divorced, there’s a higher chance of them trying different kinds of beer (and of course, more beer). And what’s the most major life change there is? No prizes for guessing (especially since I let the cat out of the bag in the title) – it’s the birth of a child.

Given the sea change in lifestyle that occurs with the birth of a child, new or expecting parents are particularly flexible to changing their buying behavior – more than any other consumer segment. As a result, they are a gold mine for retailers.

[Tweet “Pregnant and new mothers are the holy grail for retailers”]

They buy a lot of new products – diapers, wipes, cribs, prams, blankets, bottles, etc. – that they haven’t bought before. Surveys in the US have shown that new parents can easily spend over $10,000 on baby items before their child’s first birthday!